To be clear, this is not an in-depth write-up on the investment case for Mastercard. That might come later. With this post, I discuss what I think are some overlooked metrics that are the result of Mastercard’s scaled payment network.

Background

Formerly an organization mutually owned by a large collection of credit card issuing banks, Mastercard went public in 2007. No longer beholden to its bank shareholders, Mastercard had free reign to maximize the long-term value of only Mastercard, and thus embarked on a long journey to do just that. Through acquisitions and reinvestment back into its business, Mastercard has continually sought to increase the value of both its payment rails and the many value-added services it provides to its customers.

Transaction Growth is the Evidence of Customer Value

I believe one of the strongest barometers for whether Mastercard is creating value for customers is whether the number of transactions on its network is increasing. If customers found little value in doing business with Mastercard, transactions would stagnate or decline, and in turn so would Mastercard’s revenues and profits.

On the metric of transactions, Mastercard has had extraordinary success.

In 2007, the total worldwide purchase transactions using Mastercard’s network was a measly 23.8 billion. In 2023 alone, Mastercard recorded an increase of 20.8 billion in the number of worldwide purchase transactions on its network, from 150 billion in 2022 to 170.8 billion.

More Cards, Less Cash

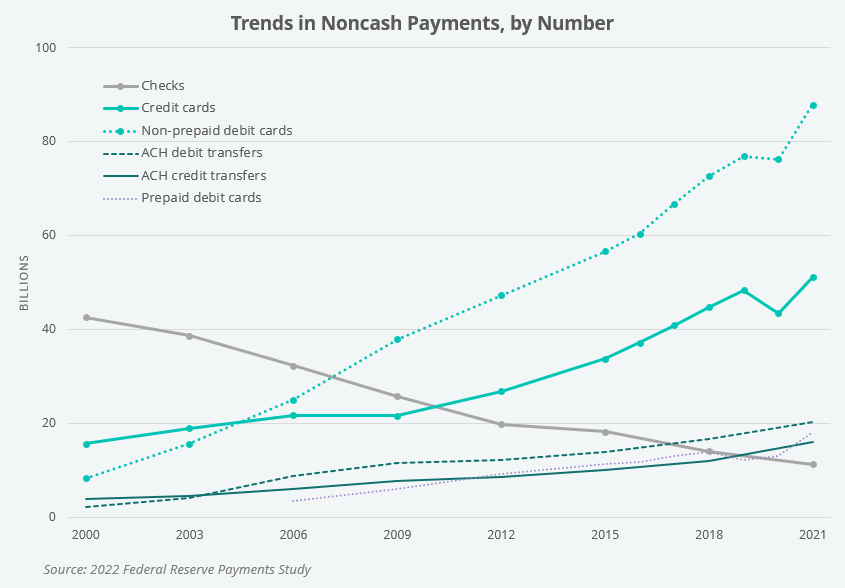

But we can’t just stop at Mastercard’s numbers. Let’s look at data from the Federal Reserve Bank of San Francisco. They’ve conducted an annual survey of consumer payment choices since 2016. The chart below shows credit and debit cards had a combined share of 45% in terms of all available payment types in the United States. In just six years, this combined figure grew to 60%.

More data comes from the 2022 Federal Reserve Payments Study. This chart shows the trends in just noncash payments by number of transactions. Again, we see a steep rise in the popularity of credit and debit cards while more traditional methods have declined or failed to keep up the pace.

Simple Explanations for Credit/Debit Popularity

There are many explanations for the increase in use of credit and debit cards, but they all boil down to utility. The increase in online shopping over the last 15 years might be the primary contributor to the popularity of cards—it’s just impossible to use cash or check to buy something online! With many credit cards, consumers also have the opportunity to earn rewards or cash back.

Advancements in payment technology is another factor. Contactless payment technology has only in the last several years become mainstream in the U.S. despite being rolled out since 2015. Thanks to contactless, debit/credit cards are even more convenient to use in-person, whether at a physical store or in an increasing number of major public transportation systems. According to Sachin Mehra, CFO of Mastercard, on July 31, 2024:

“Card present growth was aided in part by an increase in contactless penetration as contactless now represents approximately 69% of all in-person switched purchase transactions.”

Faster, easier payments drives consumers to use cards more frequently. Like having a newspaper delivered to a mailbox, the days of using cash or check will only be a memory to those of certain prior generations.

But at What Cost?

Although more transactions enables Mastercard to earn more revenues, has this translated into profits? Although customers and end users have received value from Mastercard, have the shareholders of Mastercard received adequate value in return?

The short answer is “yes”.

Over the last 16 years, through the great financial crisis of 2008-2009 and through a global pandemic, Mastercard has grown revenues from $4 billion to $25 billion and has doubled its EBITDA margins from 30.2% to 61.1%. The returns to shareholders have been equally exceptional over that time.

So how have margins doubled over this time period? The answer lies in a scaled, trusted network with a plethora of value-added services attached to it. The marginal cost to take care of an additional transaction, let alone another few million, is extremely low. Mastercard’s investment in its enabling infrastructure—we measure this as the combined spend on capex and capitalized software—stands at just 4.3% of their total 2023 revenues. The benefits of scale will continue as Mastercard spreads its costs across a growing avalanche of transactions.

Expenses Per Transaction

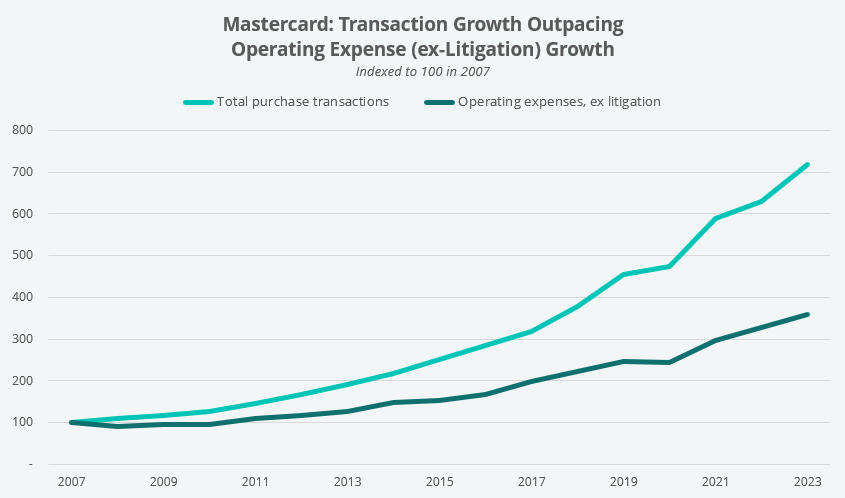

Now we are finally at the overlooked metric I find useful in illustrating how Mastercard has achieved its extraordinary margins: the reduction in its expense per transaction. It’s a more precise way of saying “economies of scale”.

The chart below shows both the total operating expense per transaction (excluding litigation provisions and charitable contributions) as well as just the processing expense per transaction. (Please note that Mastercard labels what we describe as “processing expenses” as “data processing and telecommunications” expenses).

There has been a steady, long term decline in total operating expense per transaction. In 2007, it cost Mastercard about 12.3 cents to process every transaction in its network. This declined to just 6.2 cents per transaction in 2023. In other words, transactions have grown faster than total operating expenses.

The next chart is a simulacrum of the prior chart. This one shows the growth of transactions and total operating expenses (excluding litigation provisions and charitable contributions) with both indexed to 100 in 2007. We see that transactions in 2023 were 7.2x greater than in 2007 while operating expenses were just 3.6x greater than in 2007.

We can also dive a bit deeper into some of the operating expense categories. Although growth in processing expenses have kept up with growth in transactions, one line item that has benefited tremendously from scale is marketing and advertising. In its time as a public company, the largest amount Mastercard ever spent on this line item was in 2007: a grand total of $1.1 billion (26.6% of revenues). In 2023 the spend on marketing was $825 million (3.3% of revenues). The marketing spend as a percentage of revenue has declined significantly over time, which has contributed meaningfully to Mastercard’s margin expansion.

Summary

To summarize, here’s a great passage from page 100 of Joe Nocera’s book, A Piece of the Action (published 1994), about credit cards and processing:

“It’s a complicated array of things you don’t see, but it all happens so quickly and smoothly that you don’t even think about it. Here, then, was another paradox: computers weren’t important only because they managed highly complex tasks; they were important because they disguised highly complex tasks. By making a complicated process invisible, computers allowed people to forget about the complexity, and focus instead on what was visible: namely, how easy the thing was to use.”

Payment cards have become ubiquitous thanks to convenience and ease of use. Nilson Report says there were 26.71 billion payment cards in circulation worldwide at the end of 2023. They predict that number will reach nearly 30 billion at the end of 2028. As of right now, there’s 8.1 billion people alive on this planet, so it’s amazing there is still room to grow the number of cards in circulation.

Since its IPO in 2007, Mastercard has played its part in the war on cash, investing billions to accommodate more transactions and more payment methods. As it has invested in capacity, Mastercard’s financials have benefited greatly from its growing scale and the value realized by its customers. Operating costs per transaction has halved from 2007 to 2023. We believe they will slowly decline for years to come.

Please Subscribe

You may subscribe to Doug's Substack where he posts more frequently on a wider variety of topics.

You may also subscribe to Andvari's newsletter.

Disclaimers and Notes

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

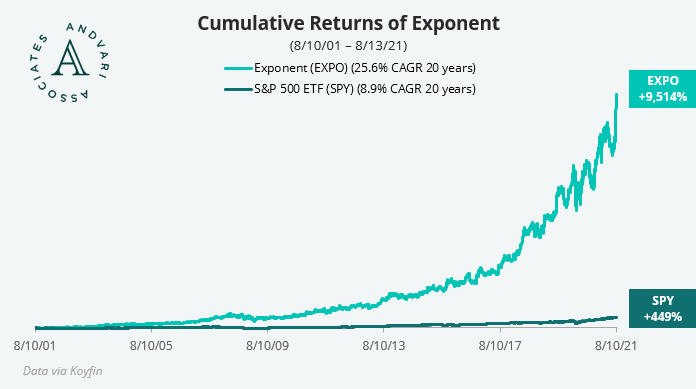

Tyler Technologies, based in Plano, TX, is the only public company focused solely on software for state and local governments in North America. Since 1998, Tyler has acquired over 40 software companies. Revenues have grown from $50 million in 1998 and will likely surpass $2 billion at the end of 2024. Cash flows and operating profits have grown at a faster rate over this time frame.

FIRST TRANSFORMATION

Although most of us know Tyler now as a pure software company, it actually started out as a manufacturing and industrial company.

The story begins with Joseph McKinney, a venture capital investor in the 1960s, who used his early financial success to start a company named Saturn Industries. McKinney acquired Tyler Pipe in 1968, a manufacturer of sewage pipes, and changed Saturn’s name to Tyler Corporation. In the ensuing two decades, McKinney used Tyler as a vehicle to acquire a variety of businesses, adhering to the M&A-driven conglomerate style of businesses in vogue during those years. Tyler ultimately hit its first peak in revenues in 1987, reaching $1 billion in sales.

In the late 1980s, McKinney saw private equity companies entering the M&A fray, doing larger and larger deals at larger and larger multiples. However, unlike many of his peers, McKinney had some discipline. Thus, McKinney began to sell most of the businesses he had acquired over the years. By the mid-90s, Tyler had sold 12 businesses and distributed over $400 million to shareholders.

However, the deal-making desire didn’t completely leave McKinney. In 1995, McKinney bought Forest City Auto Parts and Institutional Financing. These both turned out to be awful investments and McKinney resigned as CEO in 1997.

From here, with the help of Louis Waters, who had acquired a 10% position in Tyler, Tyler would sell all vestiges of its past and reallocate the capital into software businesses that served local and municipal governments.

TODAY'S TYLER

Again, today Tyler is the only publicly traded company focused solely on providing software solutions to local and state governments in North America. It is the market leader with just a 6% share in a highly fragmented market worth $35 billion. Furthermore, it is one of the vanishingly few companies that have successfully pivoted entirely from one industry to a completely new industry—from industrial conglomerate to vertical market software. (If anyone knows of other examples of companies who made such a pivot, I would love to hear about it!)

Tyler is now approaching $2 billion in annual revenues after a long and steady march. Over the years, it has acquired many companies, small and large, to round out its capabilities. It has an ERP system (enterprise resource planning), products for almost anything related courts and public safety, health and human services, tax appraisal, outdoor recreation, K-12 education, and many more.

Prior to 2019, Tyler had taken an agnostic approach to building and selling its products, deferring to the preferences of its customers. Historically, as with many software companies, Tyler offered two options to its customers. One was its on-premise option, where Tyler sold a license to its customer to install and use Tyler’s software on computer systems owned and operated by that customer. In the industry vernacular, this is an “on-prem” sales model, as its customers installed and kept the software on their own premises. The second option was for Tyler to install and host the software in datacenters owned/rented by Tyler and then charge its customers on a regular basis for use of the software. Historically, nearly all of Tyler’s customers preferred the on-prem way of doing things.

With the advent of cloud computing services from Amazon, Microsoft, and Google, most software companies have transitioned from on-prem offerings to “SaaS” offerings (i.e., software as a service). This is where the customer rents the software from Tyler who then hosts it in the cloud on someone else’s computers. Tyler then collects a rent on a regular basis. The upside to the customer is they don’t have to worry about investing in expensive hardware or investing in a skilled labor force that maintains the computers and the software. The upside to Tyler is they stand to earn 2x the lifetime revenues with a cloud deal than they’d typically earn with a standard on-prem deal.

Thus, Tyler decided to become a “cloud first” company. They announced a partnership with Amazon Web Services in October 2019 and began their second transformation, from that of an on-prem software company to one with a subscription-based business model.

SECOND TRANSFORMATION

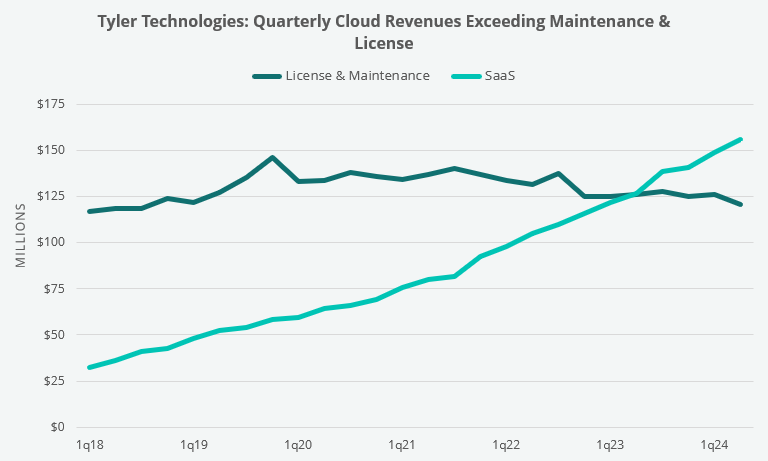

Tyler’s second transformation is now five years underway. We can clearly see that something has been going on as margins have declined from the low 20s to the high teens over the last eight years.

The cause for the decline in margins is Tyler’s transition to a SaaS business model. They’ve been consolidating the many different versions of older products. The company has also been experiencing duplicative costs as they move current customers out of Tyler’s data centers and into the cloud with AWS. Finally, the transition to a SaaS model naturally pressures margins and revenue growth because there are less up-front revenues when a customer signs a SaaS contract with Tyler.

However, we are confident Tyler’s operating margins will trend upwards to the high 20s by 2030. The primary reason is that the headwinds from the cloud transition will be gone by that time. In 2030, most of Tyler’s revenues will be from cloud and SaaS arrangements.

To measure the progress of Tyler’s transition, we track new subscription contracts as a percent of total new contracts. On a dollar value basis and on the basis of absolute number of new customers, the choice has been overwhelmingly for the cloud over the last several years.

Tyler is also flipping hundreds of current on-prem customers to the cloud every quarter. Tyler also just reported two consecutive quarters of more than 200 new SaaS arrangements with customers.

Furthermore, as of a year ago, Tyler’s quarterly revenues from SaaS arrangements have started to exceed the combined revenues from maintenance and license deals. With negligible growth in maintenance revenues ceasing to be a headwind, the tailwind from SaaS arrangements will only increasingly be felt as the company moves forward.

Finally, our last chart shows the long term shift in segment revenues. It’s plain to see the drastic move from maintenance to subscription-based revenues over the last ten years.

SUMMARY

As Tyler stated in its 2023 Investor Day presentation, they have thus far flipped about 15% of its on-prem customers to the cloud. Their goal is to increase that cumulative amount to 75%-85% by the end of 2030.

With its recent 2Q 2024 results confirming the strong trend of more current and new customers choosing the cloud and SaaS offering, we believe Tyler is on track for its audacious, long-term goal of drastically improving gross and operating margins and attaining $1 billion of annual free cash flows by the end of 2030.

Git along, little dogie.

Disclaimers and Notes

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Below is our latest letter to clients. Please share and enjoy.

Dear Friends,

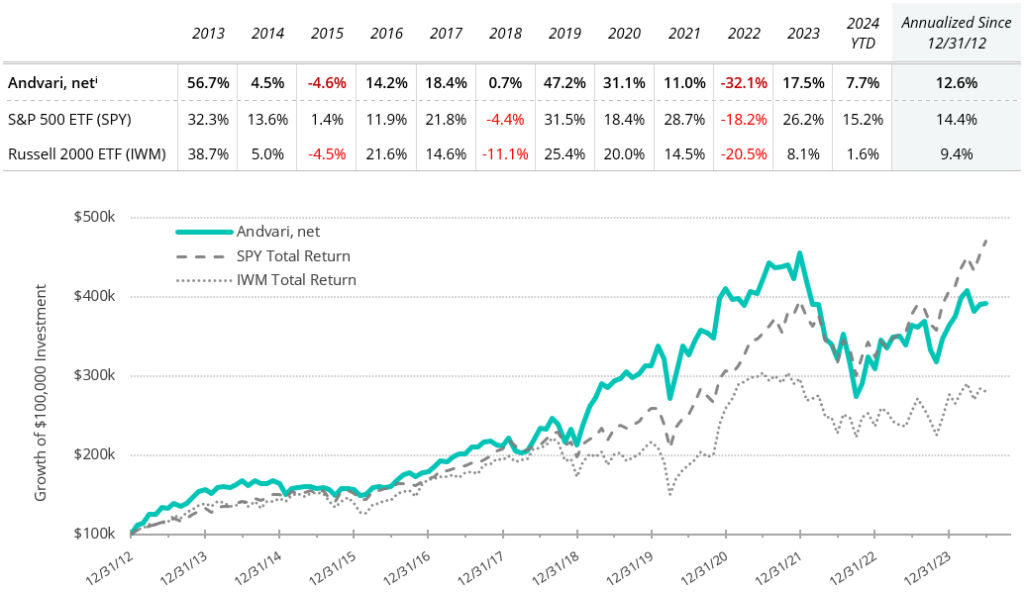

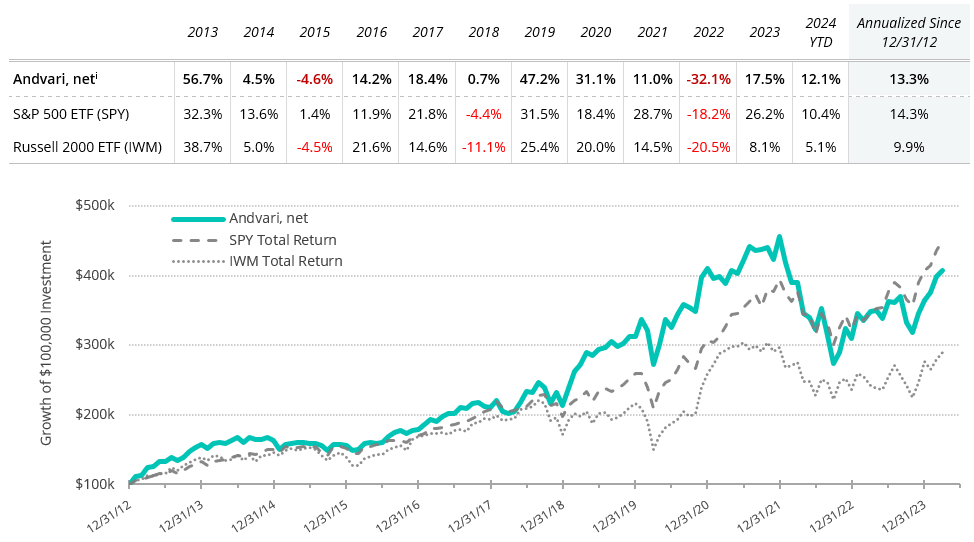

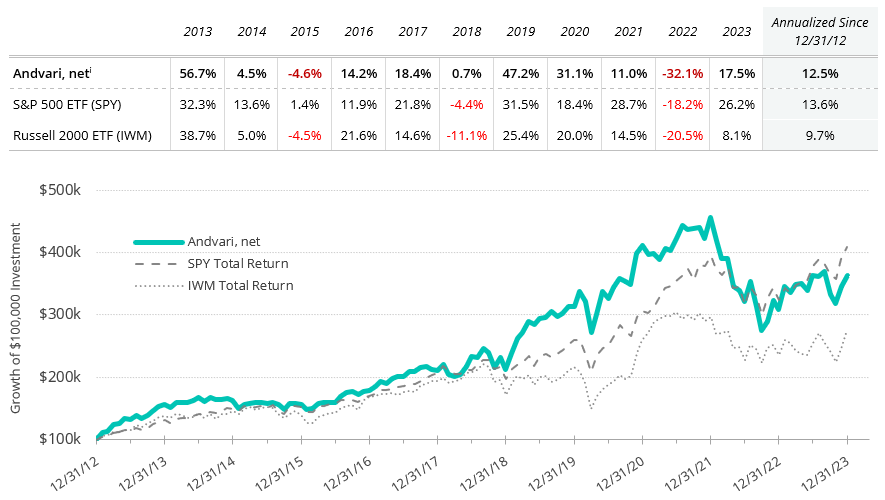

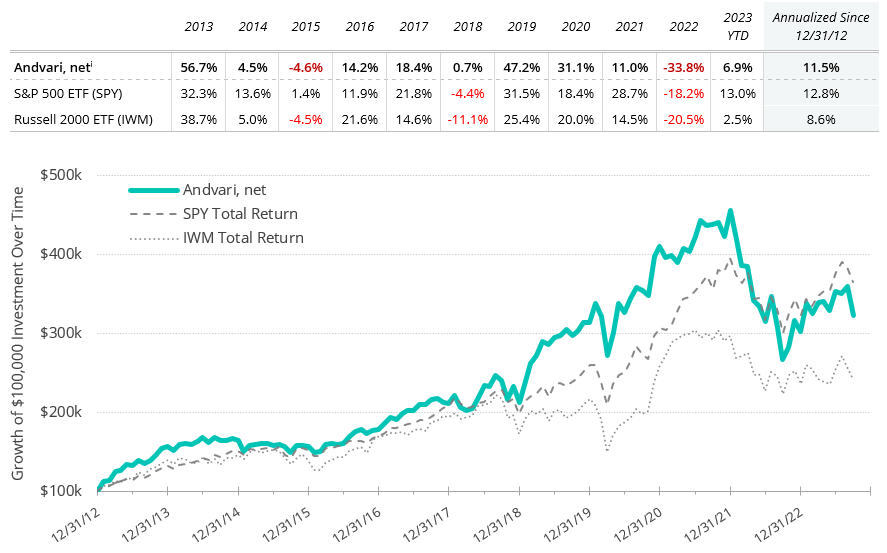

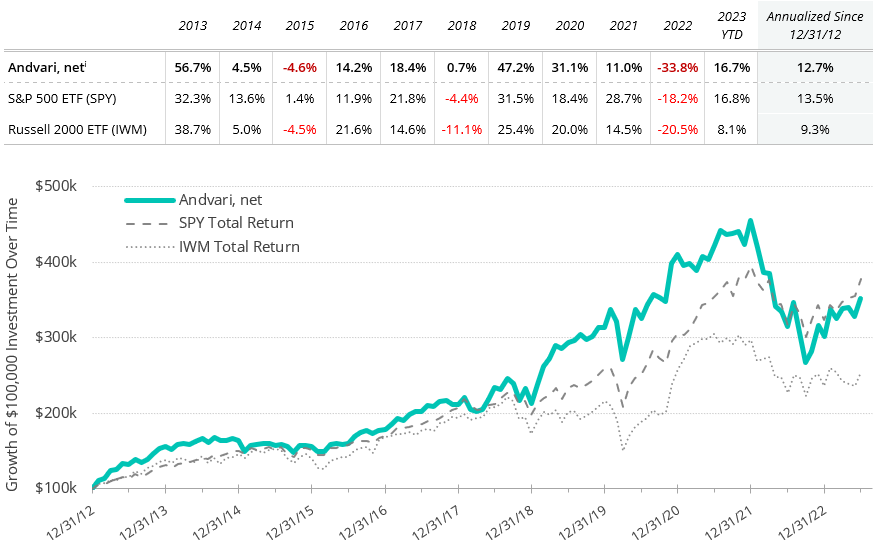

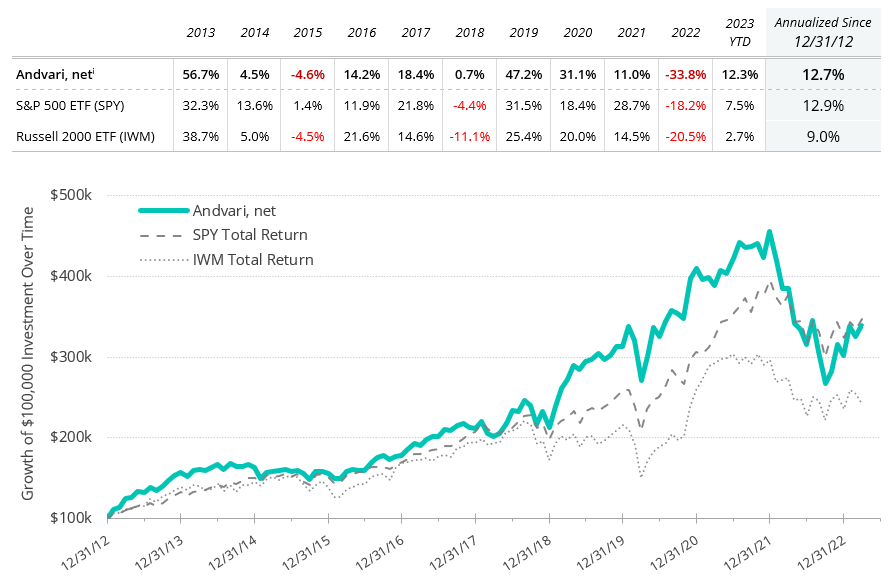

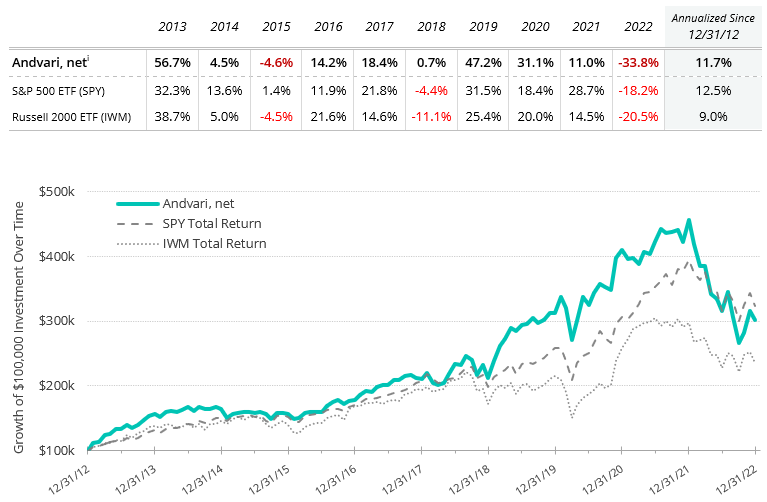

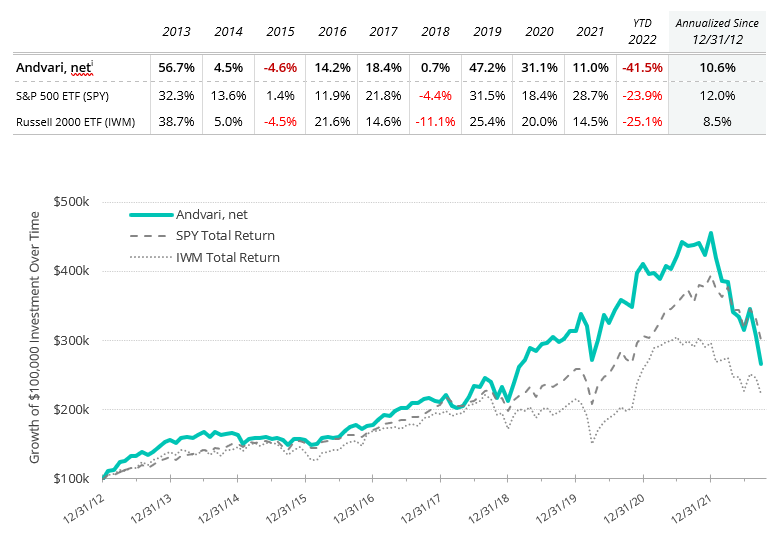

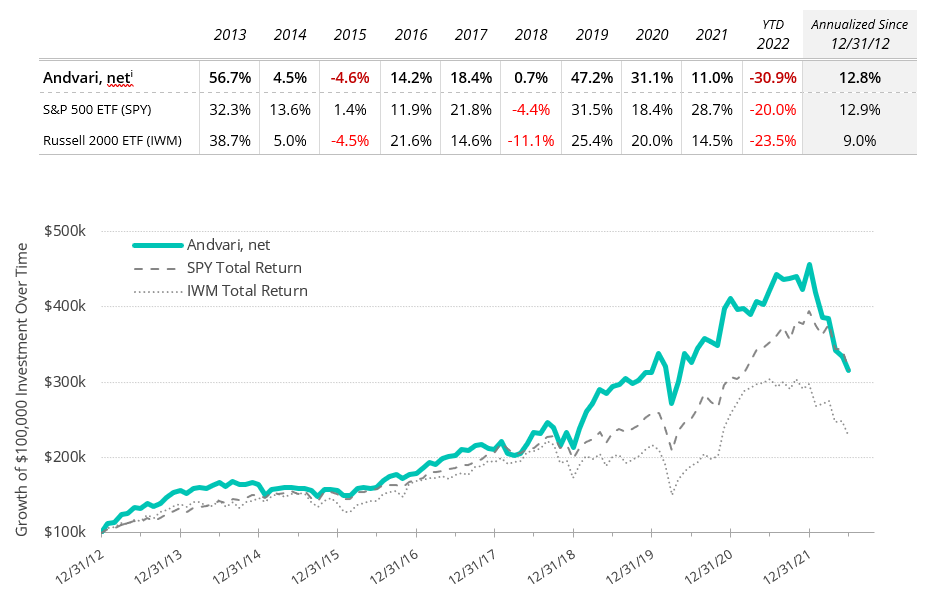

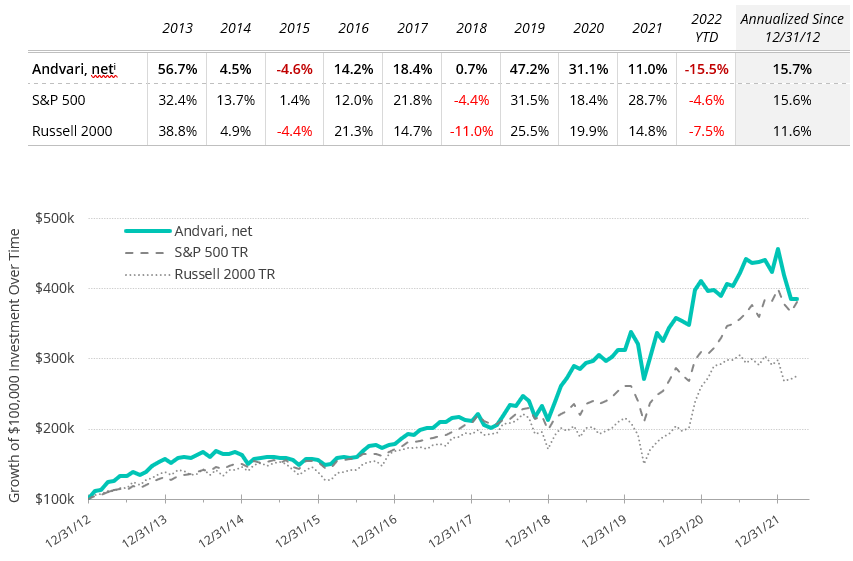

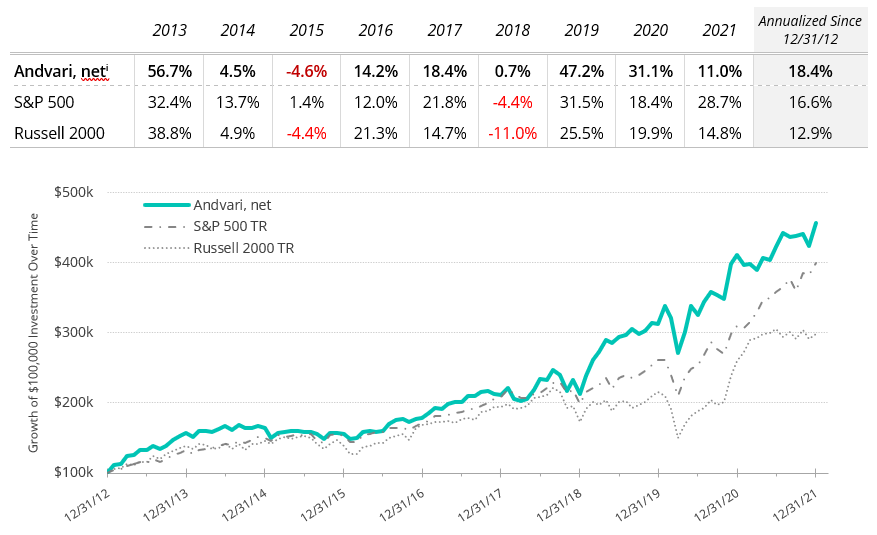

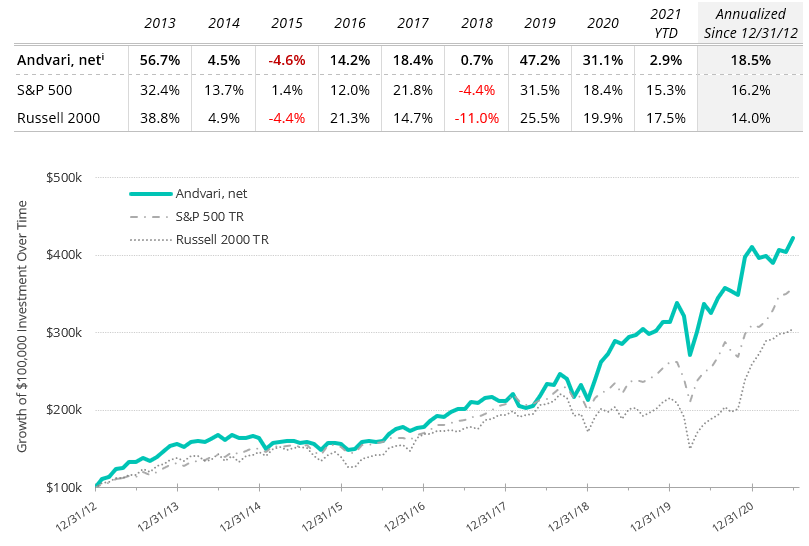

For the first quarter of 2024, Andvari was up 7.7% net of fees while the SPDR S&P 500 ETF was up 15.2%.* Andvari clients, please refer to your reports for your specific performance and holdings. The table below shows Andvari’s composite performance while the chart shows the cumulative gains of a $100,000 investment.

The main reasons for Andvari’s lagging returns are twofold: (1) Andvari has not owned some of the largest and best performing companies such as Nvidia, Apple, Microsoft, Google, Meta, and Amazon; and (2) the poor performance from Mesa. To put Andvari’s performance in better context, it’s important to know we are invested in a wide range of companies in terms of market cap. We’ve owned, or currently own, companies valued at hundreds of millions to billions and tens of billions to hundreds of billions. Given the performance of the small cap Russell 2000 index ETF (up 1.6% for the first six months) and the performance of the large and mega cap S&P 500 index ETF (up 15.2%), it is reasonable that Andvari’s performance is somewhere in the middle at this moment in time.

It’s also worth noting that Andvari’s performance in just the first six months of the year is in line with what the market on average produces in a full year, which is nothing to sneeze at. But when compared only to the higher performance of the large caps, it can feel disappointing.

ANDVARI HOLDINGS

Andvari sold out of two holdings, the largest of which is Mesa. Mesa was one of our longest held investments at the time we sold. It had performed well up until the end of 2021. Unfortunately, we held on too long. Management made two large acquisitions, one before and the other during the COVID era. It eventually turned out they paid too much for both, which does not speak well of their ability to allocate capital.

Mesa later announced in June it would delay the filing of its annual audited financial statements. A significant part of Andvari’s investment thesis was that Mesa could transition from a small-cap company run in a small-cap way to a mid- to mid-cap company run in a more professional manner. After failing to file one of its most important documents in a timely manner, Andvari felt—regretfully—some vindication we decided to cut bait and throw our line out for better fish. Thinking about what Andvari could have done differently, we likely would have made the same investment given what we knew at the time, but we should have made it a smaller position.

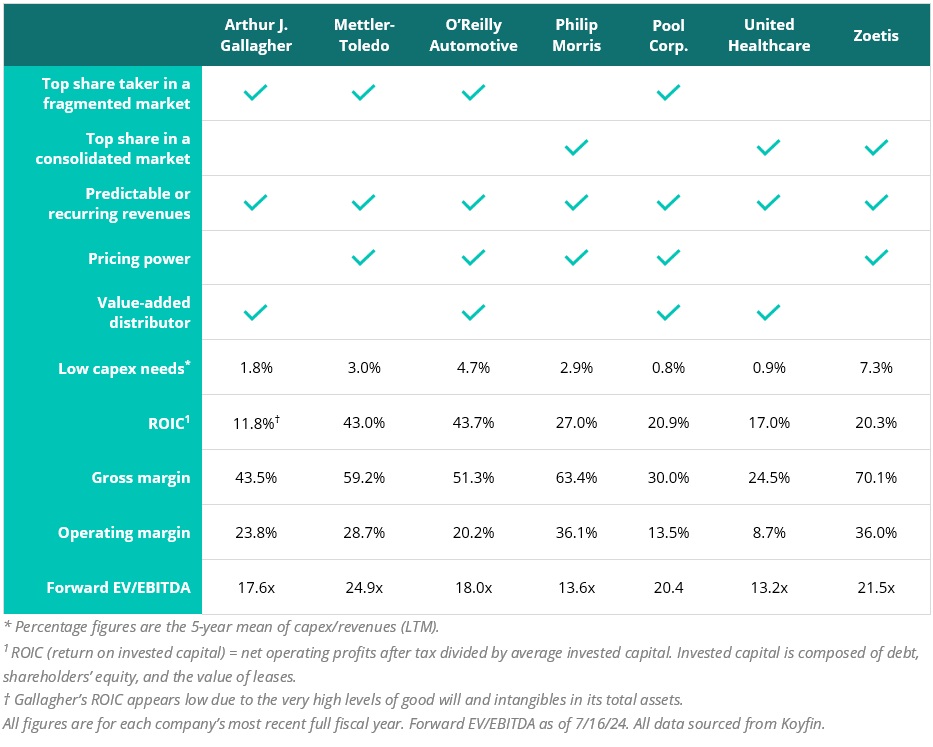

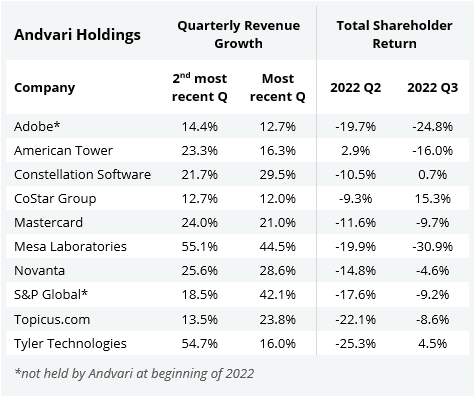

With a large amount of capital to redeploy, we started positions in a handful of companies we’ve followed for years. The table below shows how Andvari views some of the qualitative and quantitative attributes of these companies. We also give a brief overview of each company in the remainder of our letter.

ARTHUR J. GALLAGHER

Founded in 1927 by Arthur J. Gallagher, the eponymous firm is now the third largest retail property and casualty insurance broker in the United States and also the third largest reinsurance brokerage firm in the world. In addition to their brokerage businesses, Gallagher is a significant player in third-party claims administration and HR & benefits consulting.

As hinted in the above table, Gallagher is an acquisitive company. It has been a major consolidator of the highly fragmented market of insurance brokers for decades. In just the past five full years, Gallagher has acquired 195 businesses. And the market still remains fragmented. The company estimates there are tens of thousands of independent firms across the English-speaking countries of the world.

Given Gallagher’s ability to grow organically, grow through acquisition, and the essential services it provides, there have only been three times in the past twenty-five years when revenues declined: down 0.56% in 2005, down 0.31% in 2008, and down 1.63% in 2020. Which is to say, revenues barely budged despite those tumultuous years. This is a resilient company.

METTLER-TOLEDO

Mettler-Toledo makes a variety of lab instruments as well as weighing scales for industrial and retail use. These products are essential to the end users and often required to comply with a variety of regulations. The company has the number one product in most areas where it competes. However, its market share ranges from 25% to 30% share in these business lines. This means, despite its top status, competition remains highly fragmented, which gives them opportunity to capture more share over time.

With an installed base of over $16 billion worth of machines across the world, revenues from services and consumable adds to the predictability of total revenues. Pricing power is strong given the high value and relatively low cost of their products to end customers. Mettler has consistently captured 200 basis points (or greater) of net pricing every year. The company even successfully raised prices during 2009.

O'REILLY AUTOMOTIVE

O’Reilly is the third largest auto parts retailer in the country with over 6,095 stores in North America and Mexico. Their sales are split 60% to people who want to repair their own car and 40% to professionals who fix and maintain cars for a living. Following the common theme, O’Reilly sells essential products that people will buy regardless of the state of the economy.

We love that this business gushes cash—it had an extraordinary return on invested capital of 43.7% in 2023. O’Reilly has also had negative working capital since 2017, which means customers pay O’Reilly before O’Reilly needs to pay its suppliers. Looking at its capex, O’Reilly does have a higher capex ratio when compared to the others in the table. However, the ratio is still quite low considering O’Reilly is growing its store count in the range of 150-200 per year. At this rate, O’Reilly is expanding its store count by about 3% annually. Also driving the recent increase in capex has been a shift towards owning their stores rather than leasing them.

PHILIP MORRIS

Andvari invested in Philip Morris a few months after initiating a position in fellow tobacco company Altria. The tobacco industry is one that has consolidated to only a handful of players. For decades, the industry has more than offset the continual decline in cigarette volumes with price increases. More recently, both Altria and Philip Morris have introduced several new product categories that deliver nicotine in much safer ways: vaping, nicotine pouches, and heat-not-burn products. Nicotine pouches in particular continue to have an extraordinary growth trajectory. In the most recent quarter, the volumes of Altria’s On! pouches and Philip Morris’ Zyn pouches continued their torrid growth rates at 30%+ and 70%+ year over year, respectively.

For Philip Morris and Altria, their margins are high, returns on equity and capital are high, and both trade at what Andvari views as cheap or very cheap multiples. Given the non-zero chance of a “nicotine renaissance” aided by less harmful products, we do not think the future for these companies is as dim as the market seems to think.

POOL CORP

Pool is the largest player in a niche market. They are a value-added distributor of all materials and equipment related to the maintenance, remodeling, and construction of swimming pools. Although they have an estimated 40% market share, the market remains highly fragmented, which means they can grow at an above average rate organically and via further acquisitions.

In general, Pool operates in an industry with good tailwinds. Population migration from the north to the south, primarily by retirees, means more new pools and more remodeling of old pools. As the CEO of Pool recently said, the industry joke is that trucks move north with oranges and move south with furniture. Furthermore, once a home has a pool, this ensures a long-term annuity stream of products used to maintain that pool. These are non-discretionary purchases, because if an owner allows a pool to fall into disrepair, this negatively impacts the value of their home. Thus, Pool can easily pass on price increases to their customers.

As a value-added distributor, Pool is a conduit between over 2,200 manufacturers and over 120,000 customers that maintain and build swimming pools. They have taken on the role of trusted partner to manufacturers and end users. They ensure quick, efficient delivery of products while also minimizing the chances of products being out of stock. They have the largest and widest selection of products. They strive for the best customer service. They can advise customers on the best products to meet maintenance or construction needs. They’ve developed software and apps that make owning and maintaining pools easier. For all this, suppliers and customers have rewarded Pool with their long-term business. And the great part about the business is that pools remain a desirable addition to homes. This ensures a slow yet steady growth in their installed base, which drives non-discretionary, recurring sales.

UNITED HEALTHCARE

United Healthcare is one of the largest providers and distributors of services in the $5 trillion U.S. healthcare market. The company provides services to employers, individuals, and those eligible for Medicare and Medicaid. United’s Optum segment provides pharmacy benefit services and a slate of other insights and services to the major players in the healthcare space: physicians, hospitals, government agencies, and life science companies.

This is a company that provides essential services and has a strong wind at its back. Over two million people are enrolling in Medicare and Medicare Advantage every year. With the increase of healthcare spending every year, the value of the services and insights provided by Optum will only increase. United is a solid business with a high teens returns on its capital. After reinvesting in its businesses, United will likely return $16 billion in 2024 in the form of dividends and share repurchases off a revenue base of ~$380 billion.

ZOETIS

Zoetis was spun out of Pfizer in 2013 and is the largest company serving the animal health market. They make medicines, vaccines, diagnostics, devices, and technology solutions for their pet owners and veterinarians. Their revenues are split 65% for pet care and 35% for livestock.

The nice thing about Zoetis, and the pet healthcare market in general, is the trend of increasing pet ownership and the increasing willingness to spend more money on pets every year. When compared to overall consumer spending, spending on pets has nearly doubled since 1990. The resilience of the pet healthcare industry is particularly exceptional—the industry has never had a year of negative growth in the last 15 years. Zoetis in particular has grown several percentage points faster than the industry.

The financials of Zoetis are also exceptional. It has steady revenue growth, gross margins in the 70s, an ability to reinvest in the business at 20% returns, and is still able to return billions to shareholders with dividends and share repurchases. Despite having the highest ratio of capex to revenues in this group of new holdings, Zoetis is still very cash generative. The company generated $1.8 billion of free cash over the last twelve months off of $8.7 billion of revenues, a healthy 20% margin. In its first five years after being spun from Pfizer in 2013, Zoetis averaged 4.1% of capex to revenues. The reason for capex trending higher over the last five years is to support a slate of fast-growing new products, inventory buildups, and productivity enhancements. We believe this capex ratio will slowly come down over time as revenues come in for its newer products and as customers draw down inventories.

ANDVARI TAKEAWAY

Andvari redeployed capital into a handful of businesses which we believe will produce above average returns over the long term. Although we increased the total number of holdings in the equity portion of client portfolios (most have 21 or fewer individual names), we still maintain a high degree of concentration. Andvari’s top five equity positions continue to account for more than 50% of total assets under management.

With inflation continuing its slow decline, the probability of slightly lower interest rates by year’s end, and the eventual end to the COVID overhang for our life sciences holdings, Andvari expects better performance for many of its holdings over the coming years.

As always, I love to hear from clients and anyone else. Please contact me with your thoughts, comments, or questions.

Sincerely,

Douglas E. Ott, II

DISCLOSURES AND END NOTES

* Andvari performance represents actual trading performance of all, actual clients beginning on 4/12/13. Performance from 12/31/12 to 4/12/13 is actual performance of proprietary accounts, namely the accounts of Andvari’s principal, Douglas Ott. Andvari believes including Ott’s performance figures for the first 4 months and 12 days of 2013 is fair as he managed those accounts similarly to Andvari’s first clients. All performance, including the initial proprietary period, are net of management fees—assumed to be 1.25% per annum, paid quarterly, as currently advertised—net of brokerage commissions and expenses, time-weighted, and includes all cash and other securities. Performance includes realized and unrealized returns and excludes the effects of taxes on incurred gains or losses. Andvari does not certify the accuracy of these numbers. Performance data quoted represents past performance and does not guarantee future results.

The exchange traded funds (ETFs) are listed as benchmarks and are total return figures and assumes dividends are reinvested. The SPY ETF is based on the S&P 500 Index, which is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. The IWM ETF is based on the Russell 2000 Index, an index of 2,000 U.S. small-cap stocks. It is not possible to invest directly in an index. Because Andvari client portfolios are non-diversified, the performance of each holding will have a greater impact on results and may make them more volatile than a more diversified index. Andvari also engages or may engage in strategies not employed by the S&P 500 or the Russell 2000 including, without limitation, the use of leverage.

One may request a list of all securities mentioned or recommended for the preceding year as of the date of this letter. You may contact Andvari using the information below. Actual client results may differ from results depicted in this letter. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the loss of principal. Investment strategies managed by Andvari Associates LLC may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

The discussion of Andvari’s investments and investment strategy (including, but not limited to, current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the views and opinions of Andvari’s portfolio managers and Andvari Associates LLC, the investment adviser, at the time of this report, and can change without notice.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all of Andvari’s forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties, and other factors, most of which are beyond Andvari’s control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.

Andvari's Douglas Ott, in collaboration with Lawrence Hamtil of Fortune Financial, is pleased to release a new 14-page white paper: "Going South: Implications of Business and Population Migration". The paper brings together many of the data and anecdotes showing the trend of people and businesses migrating to the South remains firmly in place. In addition to many charts and graphs, Doug and Lawrence pulled together over two dozen quotes from a variety of executives whose businesses are benefiting from this migration. Below are a few excerpts from the collaboration.

DECADES OF BUSINESS MOVEMENT

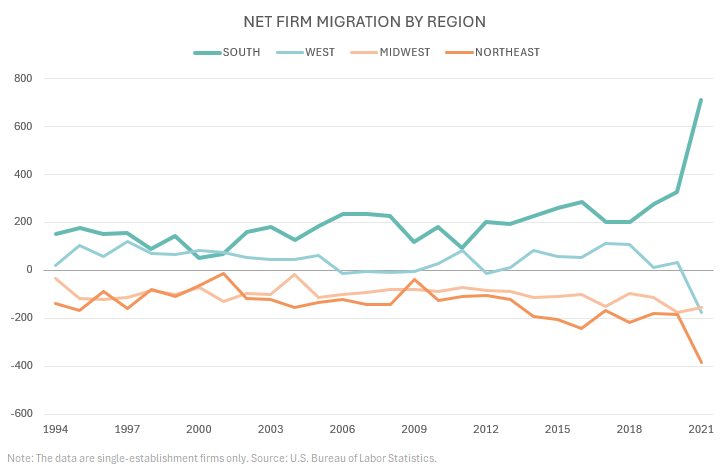

One unique dataset Doug and Lawrence found is the net migration numbers of firms moving to a new region of the country. The overwhelming benefactor has been the South for many decades.

MIGRATION CAUSES AND EFFECTS

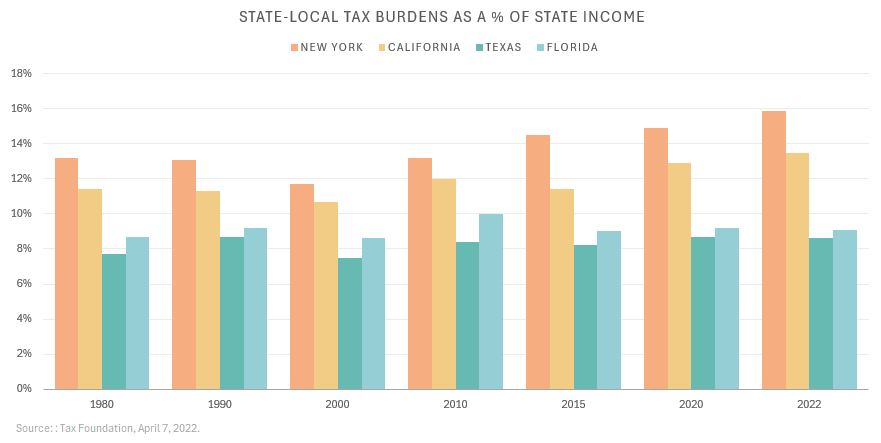

Taxes have been one reason for the migration of businesses and individuals. With the chart below, Doug and Lawrence show the large tax gap between two high tax states (California and New York) and two low tax states (Texas and Florida). Since 1980, the tax gap has only widened for these two pairs of states.

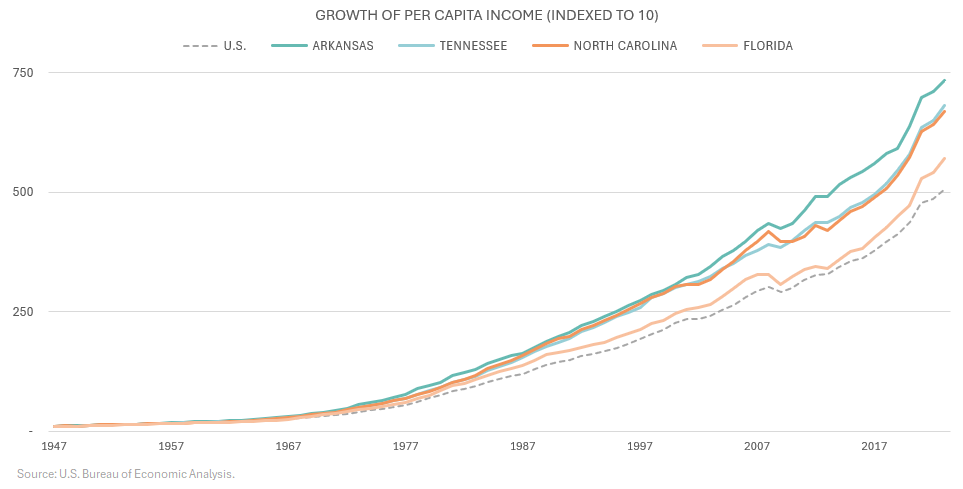

One of the many, obvious effects of migration to the South has been faster growth all around. Here you can see the per capita income levels of a handful of Southern states versus the United States since 1947. All four states have grown at a faster rate than the national average.

NOTABLE QUOTES

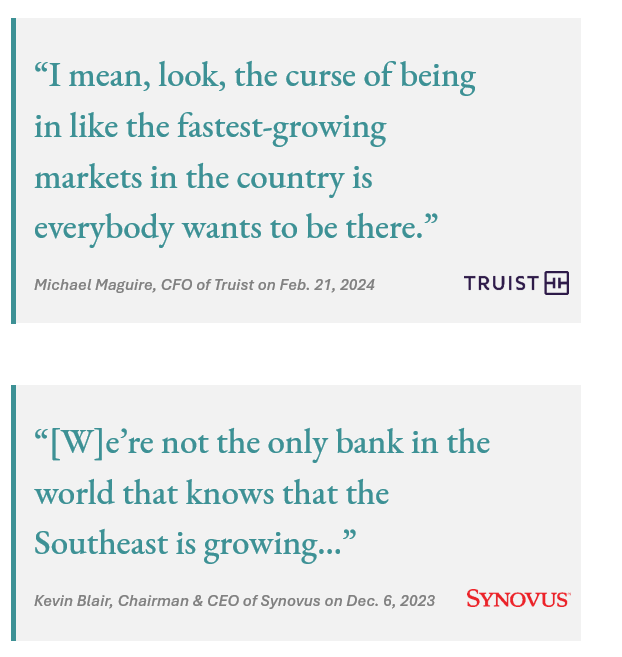

In the white paper, we have over two dozen quotes from executives commenting on the outsized opportunity they have in the South. They represent businesses in retailing, home construction, home services, infrastructure, and regional banks. Here are quotes from just two regional banks with a heavy presence in the South: Synovus and Truist.

ANDVARI TAKEAWAY

For many reasons—pro-business policies, improved infrastructure, and a milder climate—the South has enjoyed strong economic growth. The region has absorbed a large population influx from 1) simply less fortunate states and 2) states with policies inimical to business growth and productivity. This trend has persisted for several decades and it shows no signs of abating.

The long-term shift of businesses and people to the South has real implications for major industries at the national and regional level. Because of this, we believe it is important for investors to factor this major secular change into their analysis of industries and of specific companies.

Please download the 14-page whitepaperfor the full array of charts, graphs, and quotes. Feel free to share by e-mail or social media and let us know what you think!

DISCLOSURES AND END NOTES

The information herein is provided for educational purposes only and should not be construed as financial or investment advice, nor should any information in this document be relied on when making an investment decision. Andvari and Fortune have no affiliation. Opinions and views expressed herein reflect the current opinions and views of the authors, Douglas Ott and Lawrence Hamtil, as of the date hereof and are subject to change without notice.

Past performance is not a guarantee or indicator of future results. This document and the information contained herein are for educational and informational purposes only and you should not be considered a recommendation to buy or sell any particular security. You should not assume any of the securities discussed in this report are or will be profitable, or that recommendations we make in the future will be profitable. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC and Fortune Financial may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's or Fortune's current or future investments. Clients of Andvari and Fortune may own shares in any of the securities mentioned in this article. Andvari and Fortune may re-evaluate their respective holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

See the full Disclosures at the end of the white paper "Going South: Implications of Business and Population Migration".

In a recent Preferred Shares podcast, Andvari’s Chief Investment Officer and his two co-hosts continued with their series on the various industries benefiting from the construction (and continual maintenance) of the interstate highway system of the United States. In particular, the podcast focused on the early history of Vulcan Materials (VMC) and the handful of reasons of why these types of businesses are so great.

BIRMINGHAM SLAG HISTORY

The story of Vulcan begins with Birmingham Slag, a business founded in 1909 by Solon Jacobs. The purpose of the new venture was to repurpose the remnants of the steel making process for use in road construction and as ballast for railroad tracks. After years of successful operation, Jacobs sold the business in 1916 to the Ireland family.

With extreme frugality, the Irelands successfully grew the business. They opened new plants and acquired several sand and gravel pits in the southeast. With this growth, Birmingham Slag would eventually win bids on significant projects. They provided materials and services for the Tennessee Valley Authority and the Manhattan Project.

After World War II, Birmingham Slag and many other family-owned aggregates businesses had the enormous opportunity afforded them by the passage of the Federal Aid Highway Act of 1956. However, Birmingham Slag and its competitors all lacked the scale and capital to fully take advantage of this opportunity.

For Birmingham Slag, the solution was to acquire a public company called Vulcan Detinning in 1956. With this acquisition, Birmingham Slag became a public company (renamed Vulcan Materials) and could more easily raise capital. It also now had a currency with which it could acquire other aggregates businesses. For the other small players in the industry, selling to Vulcan was an attractive proposition as many were facing significant estate tax issues. They could sell to Vulcan not for cash, but in exchange for Vulcan shares, which eased their tax issues.

In four short years, Birmingham Slag transformed into Vulcan Materials, the nation’s largest producer of aggregates. Annual revenues went from $21.4 million in 1956 to $110 million in 1959 as they acquired numerous family-owned quarries.

INDUSTRY DYNAMICS

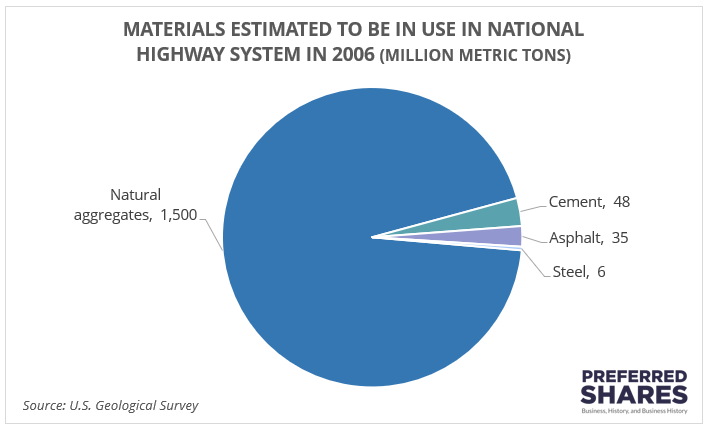

One great quality about the aggregates business is that there is no alternative to crushed rock for infrastructure and construction projects. For example, in 2006, the U.S. Geological Survey estimated that there was 1.5 billion metric tons of natural aggregates in use in the national highway system while there was just a combined 89 million metric tons of cement, asphalt and steel. Natural aggregates accounted for 94% of these total materials.

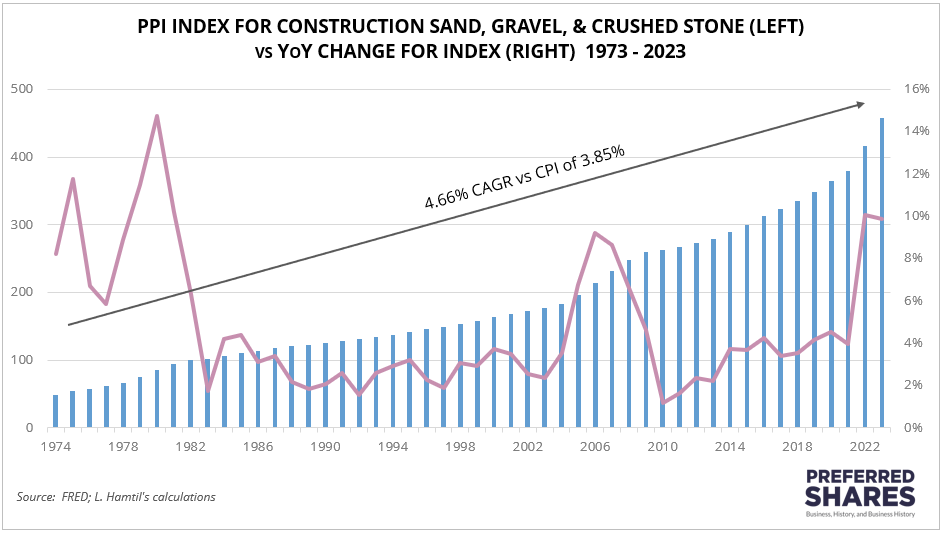

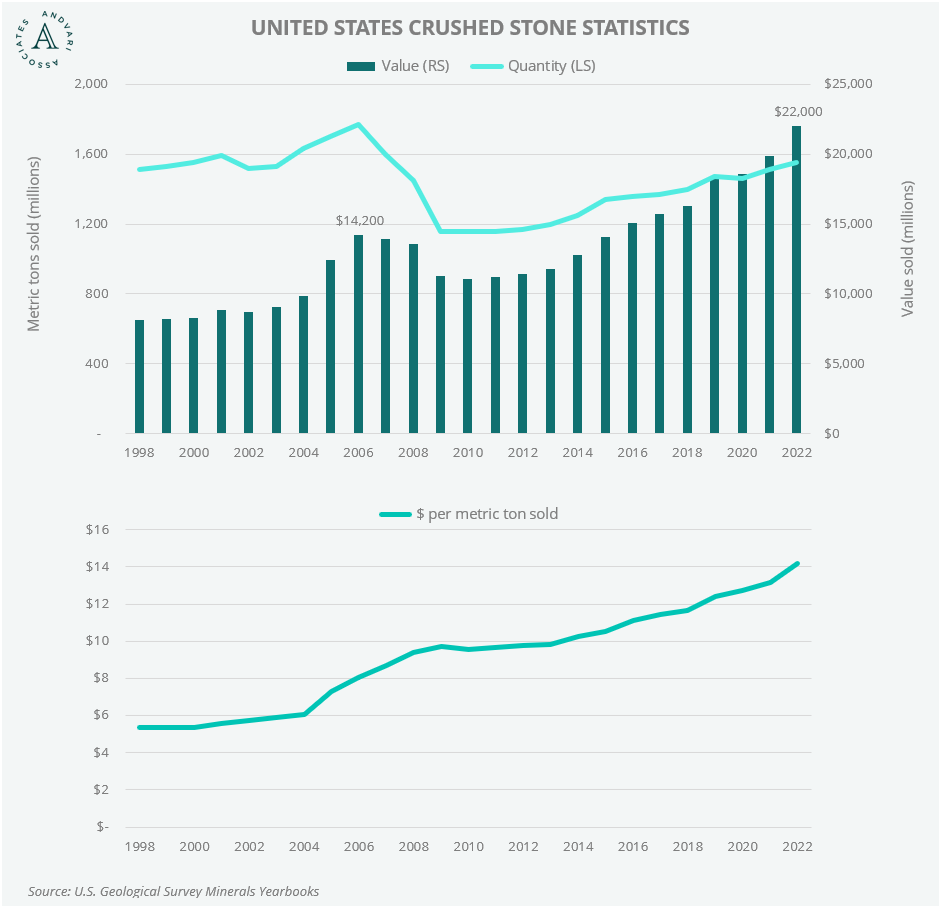

Another excellent quality of an aggregates business is its pricing power. The average price of a metric ton of crushed stone in the U.S. was $14 in 2022. However, transportation costs can quickly evaporate that purchase price based on travel distance. Thus, aggregates must be sourced locally, which gives these businesses the power to raise prices slowly and steadily above the rate of inflation. See Lawrence Hamtil's blog post “Rock Pile Riches”.

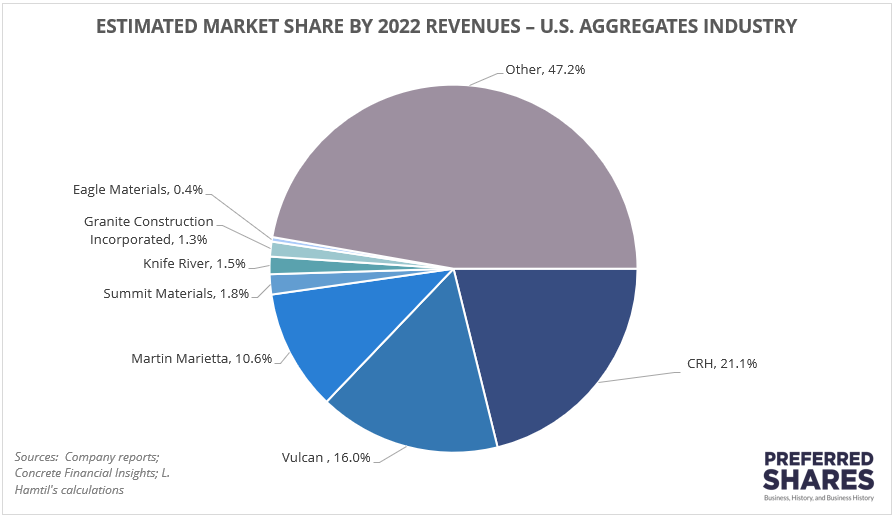

Despite several generations of consolidation, the industry remains highly fragmented. Further, the opening of new quarries is close to impossible given the permitting and regulatory hurdles. Thus, there is ample opportunity for the larger players like Vulcan, Martin Marietta, and others, to continue to consolidate by acquiring the large number of smaller players.

ANDVARI TAKEAWAY

The aggregates industry is one that will persist for many generations going forward. It exhibits many of the attributes that Andvari values. There is reliable and predictable growth from the continual spending on vital infrastructure maintenance and new construction projects. The industry has pricing power and there remains an opportunity for the large public companies to consolidate what is still a highly fragmented industry.

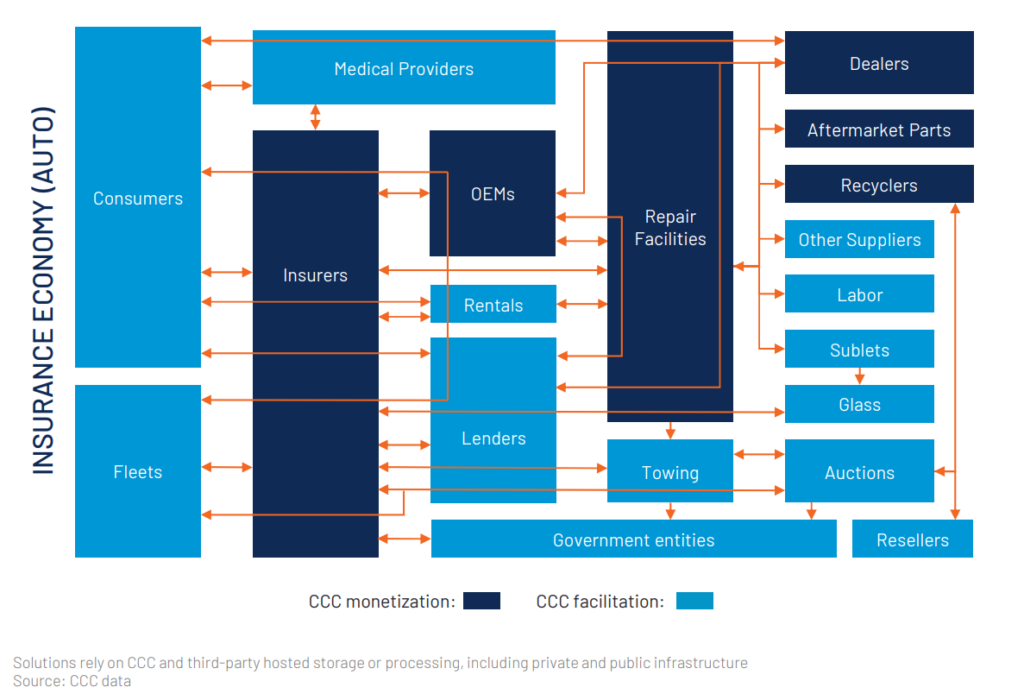

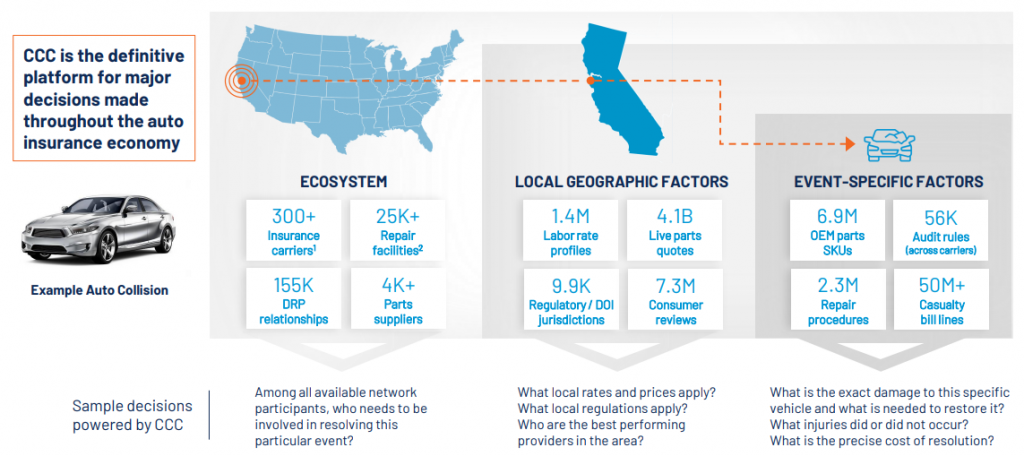

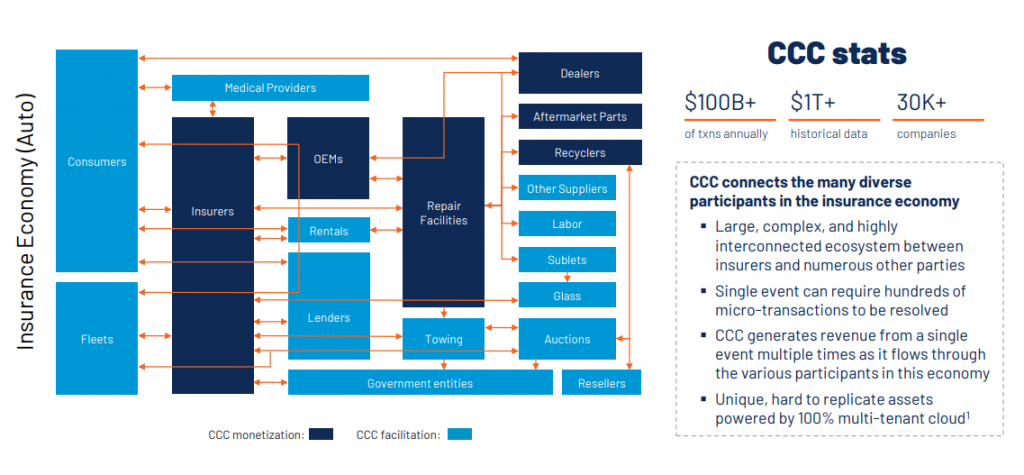

CCC Intelligent Solutions (CCCS) is a business that is central to the auto repair ecosystem. Its software helps coordinate the collective efforts of: auto insurers like GEICO and Progressive; salvage and auction companies like Copart and IAA; and repair shops such as those under the wing of Boyd Group. As part of its efforts, CCCS also collects data on over $100 billion of annual transactions in this space. It then regularly publishes a report—entitled “Crash Course”, naturally—that details all the trends affecting the auto repair journey. With their most recent “Crash Course” report, CCCS affirms that the trend of rising costs to repair a vehicle are still in place.

CCCS chart showing all the various industries involved after a vehicle accident

VEHICLE COMPLEXITY

The main trend contributing to increasing repair costs is that new vehicles continue to grow in complexity. Although complexity has allowed for vehicles that are “safer, more reliable, and more comfortable”, the average new car now has somewhere between 1,400 and 1,500 semiconductor chips and roughly 30,000 parts. Further, the electronic parts of a car now account for 40% of its total cost.

All the benefits allowed for by electronics and new material types come at a cost. These new parts and features are costlier to repair. The repair shop industry still grapples with an inadequate number of technicians who can tackle modern vehicles. Claims cycle times have increased along with costs. Thus, insurers are more and more likely to declare a car “totaled” after it’s been in an accident.

CCCS cites research from AAA regarding the repair costs that are over and above the normal bodywork required following a collision:

“ADAS-equipped vehicles can add up to 37.6% to the total repair cost after a crash due to expensive sensors and calibration requirements. Even minor incidents that cause damage to this technology found behind windshields, bumpers, and door mirrors can add up to $1,540 in extra repair costs.”

REPAIR COSTS

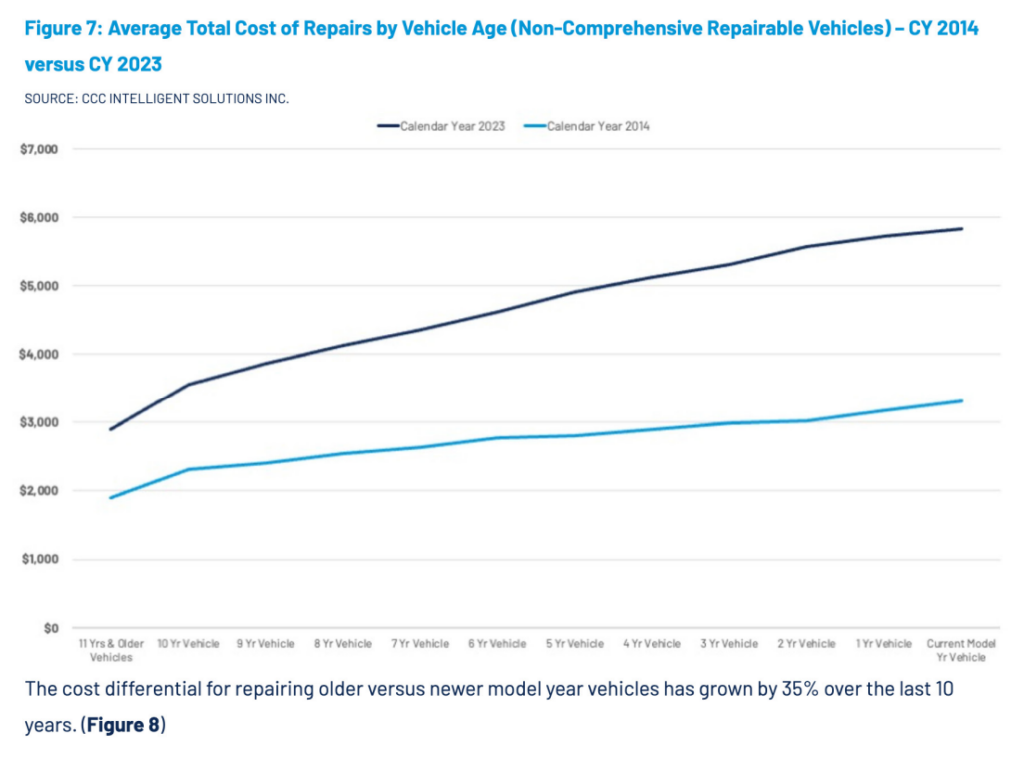

CCCS data shows that newer cars are in fact costlier to repair than older model cars. The following chart shows the average cost of repairs by vehicle age. “The cost differential for repairing older versus newer model year vehicles has grown by 35% over the last 10 years,” according to CCCS.

Tim O’Day, President and CEO of Boyd Group, confirms repair costs are higher for newer vehicles during Boyd’s 11/10/23 earning call:

“[W]e do continue to see increasing repair severity. And I would expect … that will continue over time. If we look at … newer vehicles, say, the 1- to 3-year-old range, the average repair cost of those vehicles is meaningfully higher than you would see in 4 to 7 and then 8 plus.… Newer cars are more expensive to repair anyway. But the newer vehicles also have more technology. So I think that's a trend that likely or not is more than likely to continue.”

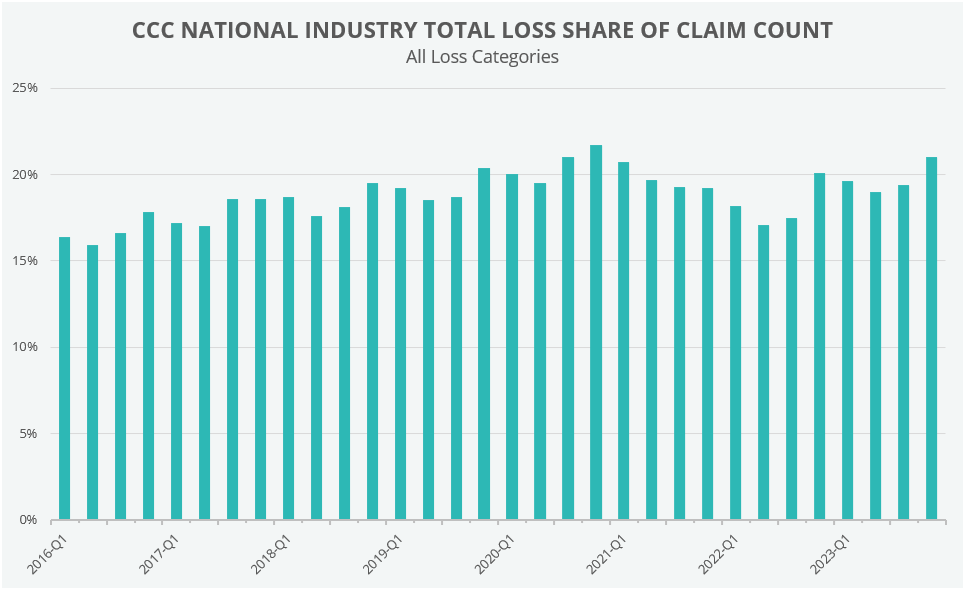

TOTAL LOSS FREQUENCY

When the total cost to repair a vehicle exceeds the value of the vehicle, the insurance company will usually deem it a total loss. With rising costs to repair, there has been a concurrent increase in the total loss frequency. The chart below shows the total loss frequency increasing from 16.4% to 21.0% over eight years.

Once the insurer deems a vehicle a total loss, this is where companies like Copart and IAA step in. They collect the vehicle with a tow truck, clean them up a bit, test whether it can drive, take some photos, and then put it up for auction on their websites for anyone around the world to bid on.

Jeff Liaw, co-CEO at Copart, has often stated that it is his and Copart’s belief that the total loss ratio will eventually reach 30% over time due to increasing vehicle complexity and repair costs. Another factor that could boost total loss frequency would be some insurance carriers abandoning their practice of repairing cars when they should not. On Copart’s 2/22/24 quarterly conference call, Liaw noted that there is also still a wide difference total in loss practices on the part of carriers:

“I think there is long-standing conventional wisdom among some folks that drivers and owners prefer to have their cars back, and … insurance companies will sponsor repairs of cars that they economically should not. So that behavior does continue in the industry. And as a result then, we see a pretty wide dispersion of total loss practices across all carriers, though virtually all of them have increased total loss frequency over the long haul. As for your question about where total loss frequency—can it exceed 30%? I think the answer is affirmatively yes.”

The auto repair ecosystem is a vital component to the logistics and mobility of any country. As such, the various players in the repair ecosystem, from the insurers to the body shops and from the salvage yards to software providers like CCCS, have a nice steady tailwind thanks to the enormous U.S. auto market. Further, all players in this ecosystem are fairly recession resistant. Despite all the new technology that makes driving safer, there will always be accidents, in good times and bad. This industry is a space in which Andvari maintains a keen interest.

DISCLOSURES AND END NOTES

Past performance is not a guarantee or indicator of future results. The opinions expressed herein are those of Andvari Associates LLC and are subject to change without notice. This document and the information contained herein are for educational and informational purposes only and you should not be considered a recommendation to buy or sell any particular security. You should not assume any of the securities discussed in this report are or will be profitable, or that recommendations we make in the future will be profitable. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari clients own shares in Copart. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Below is our latest letter to clients. Please share and enjoy.

Dear Friends,

For the first quarter of 2024, Andvari was up 12.1% net of fees while the SPDR S&P 500 ETF was up 10.4%.* Andvari clients, please refer to your reports for your specific performance and holdings. The table below shows Andvari’s composite performance while the chart shows the cumulative gains of a $100,000 investment.

ANDVARI HOLDINGS

In fits and starts, Andvari’s performance continues to climb back from the decline we suffered in 2022. The top two detractors to our performance in the quarter were Mesa Labs and American Tower. The top two contributors to performance were Topicus.com and Mastercard.

We have two holdings on which we can report several notable events. First is Kelly Partners Group, the Australia-based accounting and financial services firm. The company continues on its long-term mission of helping small businesses be better off by the provision of high-quality accounting and tax services. We’re pleased to share that Kelly has expanded into the United States. This is its first foray outside of its home country. After acquiring two accounting firms in the L.A. area, Kelly is now ranked 71 on Los Angeles Business Journal’s Top 100 Accounting Firm list. Notably, L.A. is home to one of the largest populations of Australian expatriates in the world. There are 60,000 Australian businesses in L.A. and until Kelly Partners arrived on the scene, there was not a single Australian-owned accounting firm there. This is a logical place for Kelly to begin its international expansion.

Another event, perhaps even more significant than its entry into the U.S., is its decision to eliminate its monthly dividend. This means Kelly can deploy more capital at much higher rates of return than Andvari can hope to provide. Given Kelly’s large opportunity to acquire and improve accounting firms in English-speaking countries, Andvari applauds the decision to eliminate the dividend.

Finally, as of February, the shares of Kelly Partners now trade in the U.S. via the OTCQX® Best Market. Although this is an over-the-counter market,1 Andvari believes this is a first step towards an aspirational—and perhaps eventual—up-listing to an exchange like the NASDAQ. At the minimum, Kelly can now garner more attention and support from a larger investor base. This will likely help its share price and Kelly will be better able to access capital if necessary.

CoStar Group is the second holding with significant news. As a reminder, CoStar is commercial real estate's leading provider of information, analytics, and online marketplaces. Sensing an opening to compete against Zillow, the leading residential real estate portal in the U.S., CoStar acquired Homes.com in 2021. CoStar is now planning to invest a cumulative $1 billion into this new business segment. Part of this investment will include the largest marketing campaign in the history of the residential real estate industry. If you watched the Super Bowl this year, you likely saw one of their four commercials. Homes.com will be a big advertiser at other major events in 2024.

Thus far, these investments have resulted in Homes.com going from an insignificant player to the second-most trafficked homebuying portal. CoStar announced the Homes.com Residential Network reached more than 149 million unique visitors in February. Further, Homes.com itself had a 567% year-over-year increase in traffic. As it did with Apartments.com, CoStar believes it can grow the unaided awareness from the low single digits to more than 50%.

CoStar then received news that could be a tailwind to its Homes.com business: the National Association of Realtors reached a $418 million settlement of claims that they and the industry conspired to keep real estate agent commissions high. The practice of two agents sharing a commission based on the value of a home is a big reason why commission rates in the U.S. are among the highest in the developed world. The practice also reduced the ability for the home buyer to negotiate on commissions. The commission sharing practice is also why many buyers’ agents steered clients away from homes when the shared commission would be lower than the going rate. Thus, as part of the settlement, the NAR agreed to disallow upfront commission offers from sellers’ agents to buyers’ agents.

The reason this settlement could provide a tailwind to Homes.com is because its business model is geared to the sellers’ agent. This contrasts with the business models of portals like Zillow and Realtor.com, which are geared towards taking the listing data from the sellers' agents, generating leads, and then selling those leads to buyers' agents. Understandably, this practice has been hated by sellers' agents for a long time. Thus, if the commissions of buyers' agents decline because of the changes stemming from this settlement, Zillow could suffer and Homes.com could increase its market share.

SILVER LININGS IN RATES

Although the rapid rise in interest rates contributed to Andvari’s underperformance in 2022, there are silver linings to rates having risen to more normal levels. One benefit is the opening of new opportunities to invest in businesses whose market values have declined too much. The other benefit is pure and simple: the yields on assets like bonds, preferred shares, and certain equities, are at levels finally worthy of notice.

One example of an attractive yielding asset is a bond fund Andvari has used for our clients who desire an income component to the equity strategy Andvari provides. This fund is the Western Asset Premier Bond Fund (WEA) managed by Western Asset Management, an advisor founded in 1971 in Pasadena, CA. We like the group for its value investment approach and its long-term track record in the fixed income arena. Furthermore, Western has an excellent reputation and a historical association with two extraordinary individuals: Lou Simpson and Ron Olson.

Lou Simpson is best known for his long career as the person in charge of GEICO’s investment portfolio. Warren Buffett’s Berkshire Hathaway owned a large stake in GEICO until it fully acquired the business in 1996. With the GEICO acquisition, Buffett acquired both a great business and great people. In his 2004 letter to Berkshire shareholders, Buffett wrote, “Lou is a cinch to be inducted into the investment Hall of Fame.”

What few people remember is Simpson was CEO of Western Asset prior to GEICO luring him away. Although Simpson’s tenure at Western was brief, he was attracted to the group for a reason. We believe at least a small part of his investment philosophy remains embedded within Western.

Ron Olson is the other person of note. Olson has a long association with Charlie Munger and Berkshire Hathaway. In 1968, Olson joined the law firm founded by the late Munger, which is now named Munger, Tolles & Olson. He has been a director on the board of Berkshire Hathaway since 1997. Olson has also been a director at Western Asset since 2005. It’s hard to imagine a better person to be a director on your board than Olson.

Now, getting to some of the specifics on WEA. It is a bond fund with a closed-end format. This means it has a fixed number of shares as opposed to the open-end fund format, which issues new shares to each new buyer. A closed-end fund also means its market price can trade at a premium or a discount to the net asset value (NAV) per share of the fund. In other words, we are frequently able to pay $95 for WEA shares that have a NAV of $100. The converse is also true. We might be able to sell shares at prices greater than the NAV. Currently, the fund has a yield of 7.9% on its market price in addition to trading at a ~6% discount to NAV.

SMOKE SIGNALS

Our second example of a high-yielding security is the stock of Altria Group. Before we get into the details of why we started a position in Altria, a brief history is in order. The company was formerly known as Philip Morris before rebranding to Altria in 2003. Cynically, the rebranding was to minimize the negative attention from its tobacco business. However, the company also owned Kraft Foods and Miller Brewing, so it was logical to reflect its status as a conglomerate. Since rebranding, Altria has slowly “de-conglomerated”. It spun out Kraft in 2007. It spun out Philip Morris International in 2008. In 2021, it sold its Ste. Michelle Wine Estates business. Finally, last month Altria announced it is selling part of its 10% ownership in Anheuser-Busch InBev (BUD).2

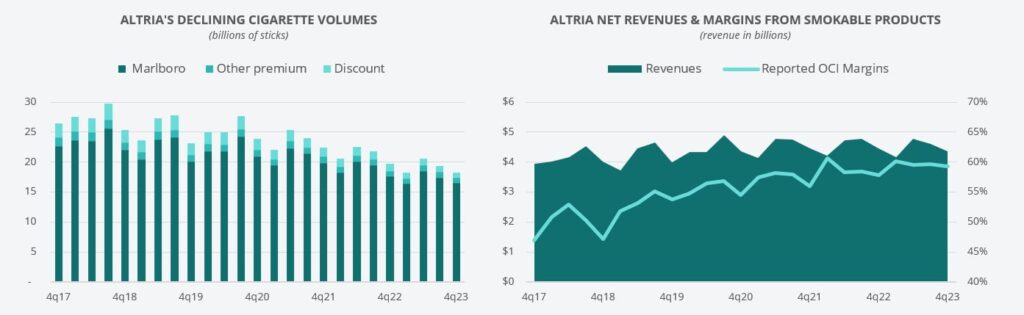

Andvari has followed Altria since we began our investment career. Profitability is extraordinary and the business requires minimal capital expenditures. Despite the volume of cigarettes having steadily declined—a great thing for our population health—Altria has still managed to grow revenues and profits with regular price increases.

Also offsetting the decline in Altria's cigarette business is the growth of its oral tobacco portfolio. Altria, and nearly all other tobacco companies, have developed or acquired multiple next generation products that deliver nicotine in a vastly safer way than cigarettes.3 These reduced risk products continue to grow rapidly. For example, Altria's on! brand of nicotine pouches is growing volumes at an annual rate of >30%. Over a long period of time, the reduced risk products will make up most of the revenues and profits for Altria and other tobacco companies.

As to why Andvari started a position in Altria, it boils down to a combination of a business with excellent qualities and simple math. Andvari likes the business for its high margins, low capex requirements, and predictable revenues. The business also has extraordinary pricing power arising from its addictive products—a nice hedge against inflation.

Then there’s the welcome news of Altria raising cash from its BUD stake (roughly $2.1 billion if they obtain an average selling price of $60 per share for BUD) it will use to repurchase its shares. This is a rational choice because Andvari believes Altria shares are undervalued. Further, with fewer outstanding shares, Altria will have smaller total dividend payments to shareholders.

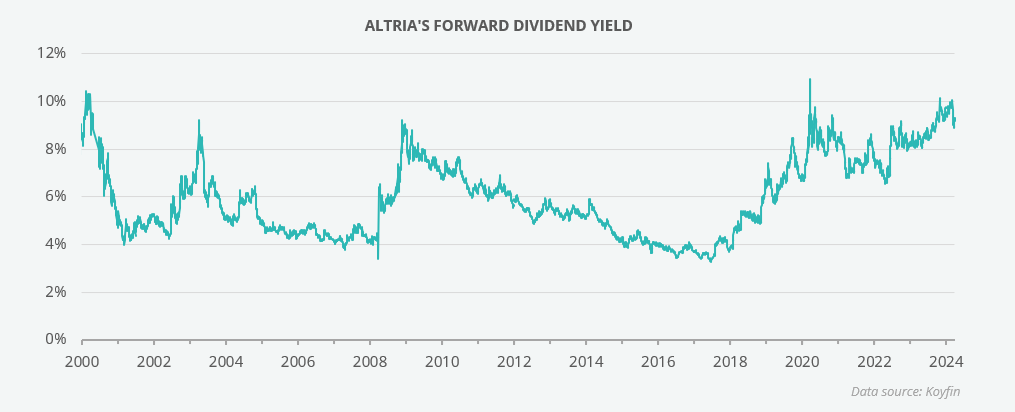

The math behind our purchase is simple. The dividend yield on Altria shares was at a level seen only two other times since the year 2000. Thus, Andvari purchased a security at a 9.7% dividend yield that can grow its dividend per share at an annual rate of 2%–3%. The odds are with us this type of investment will provide good long term returns.

ANDVARI TAKEAWAY

We're pleased to report positive results for this quarter and the positive developments at Kelly Partners and CoStar. The businesses within our investment portfolio continue to focus on their respective opportunities and all the things within their control. In the short term, the rapid rise in interest rates negatively impacted the market prices of many securities, but at the same time, it opened new investment opportunities for Andvari.

Over the long term, Andvari remains optimistic we can provide investment results that will make a difference for our clients. We intend to do this by investing in great businesses with great managers that have ample opportunities to deploy capital at high rates of return.

As always, I love to hear from clients and anyone else. Please contact me with your thoughts, comments, or questions.

Sincerely,

Douglas E. Ott, II

DISCLOSURES AND END NOTES

* Andvari performance represents actual trading performance of all, actual clients beginning on 4/12/13, managed under the primary Andvari investment strategy. Performance from 12/31/12 to 4/12/13 is actual performance of proprietary accounts, namely the accounts of Andvari’s principal, Douglas Ott. Andvari believes including Ott’s performance figures for the first 4 months and 12 days of 2013 is fair as he managed those accounts similarly to Andvari’s first clients. All performance, including the initial proprietary period, are net of management fees—assumed to be 1.25% per annum, paid quarterly, as currently advertised—net of brokerage commissions and expenses, time-weighted, and includes all cash and other securities. Performance includes realized and unrealized returns and excludes the effects of taxes on incurred gains or losses. Andvari does not certify the accuracy of these numbers. Performance data quoted represents past performance and does not guarantee future results.

The exchange traded funds (ETFs) are listed as benchmarks and are total return figures and assumes dividends are reinvested. The SPY ETF is based on the S&P 500 Index, which is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. The IWM ETF is based on the Russell 2000 Index, an index of 2,000 U.S. small-cap stocks. It is not possible to invest directly in an index. Because Andvari client portfolios are non-diversified, the performance of each holding will have a greater impact on results and may make them more volatile than a more diversified index. Andvari also engages or may engage in strategies not employed by the S&P 500 or the Russell 2000 including, without limitation, the use of leverage.

One may request a list of all securities mentioned or recommended for the preceding year as of the date of this letter. You may contact Andvari using the information below. Actual client results may differ from results depicted in this letter. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the loss of principal. Investment strategies managed by Andvari Associates LLC may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

The discussion of Andvari’s investments and investment strategy (including, but not limited to, current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the views and opinions of Andvari’s portfolio managers and Andvari Associates LLC, the investment adviser, at the time of this report, and can change without notice.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all of Andvari’s forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties, and other factors, most of which are beyond Andvari’s control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.

Brokerage firm Schwab describes over-the-counter securities as ones “that are not listed on a major exchange in the United States and are instead traded via a broker-dealer network, usually because many are smaller companies and do not meet the requirements to be listed on a national exchange.”[↩]

South African brewer SAB acquired Miller in 2002 to form SABMiller, with Philip Morris retaining a 36% ownership share. In 2015, Anheuser-Busch InBev acquired SABMiller.[↩]

Nicotine itself is not the primary cause of smoking-related diseases. The smoke produced by the burning of a cigarette contains over 6,000 chemicals, of which 100 have been classified as causes or potential causes of smoking-related diseases such as lung cancer, cardiovascular disease, and emphysema. Thus, tobacco companies have created products that do not require the burning of tobacco to deliver nicotine. Altria has research showing the reduction of harm in their smokeless tobacco, heated tobacco, and e-vapor products.[↩]

Below is our latest letter to clients. Please share and enjoy.

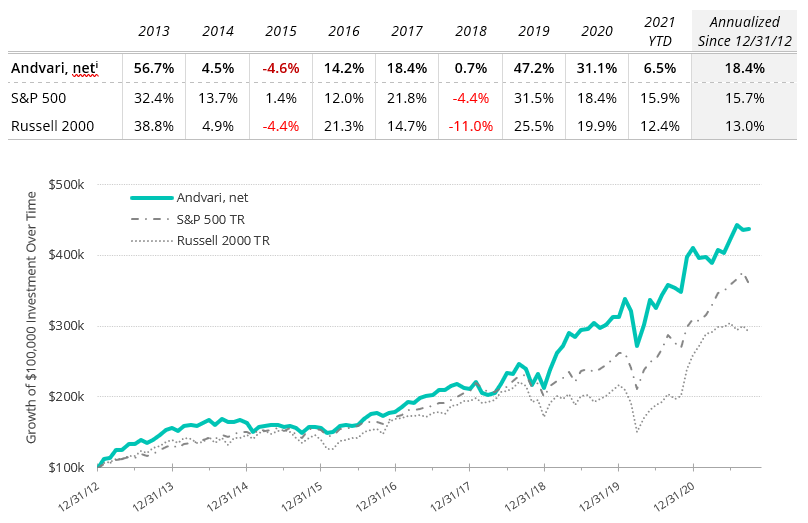

For the full year of 2023 Andvari was up 17.5% net of fees while the SPDR S&P 500 ETF was up 26.2%.* Andvari clients, please refer to your reports for your specific performance and holdings. The table below shows Andvari’s composite performance against two benchmarks while the chart shows the cumulative gains of a $100,000 investment.

ANDVARI HOLDINGS

Looking at the holdings which we held at the beginning of 2023 and that remained at the end of the year, there was a wide mix of good and bad performers. The worst performing holding was Mesa Labs whose shares had a total return of -36.7% for the year. The reasons for poor performance remain the same. First, they lost a significant customer in their Clinical Genomics business. Second, Mesa and the life sciences industry in general continued to experience the negative effects of customers de-stocking the inventories they had built up after the pandemic. Likely third and fourth reasons are higher interest rates and the overhang of Mesa’s $173 million worth of convertible debt which comes due in 2025. Mesa has the option of satisfying this debt either through issuing new common shares, with cash, or some combination of both. Neither are great options right now. Issuing new shares at low prices will excessively dilute shareholders. If Mesa wants to refinance this debt, they would be doing so at a much higher rate.

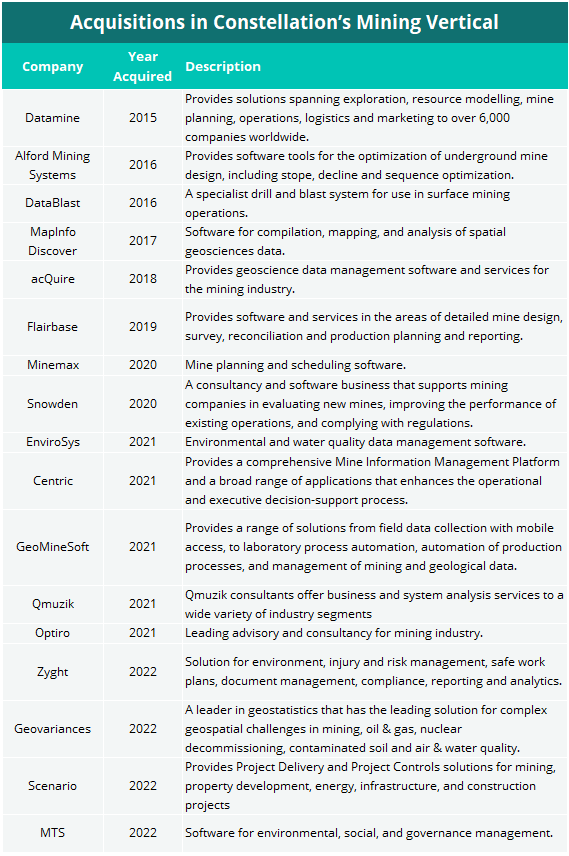

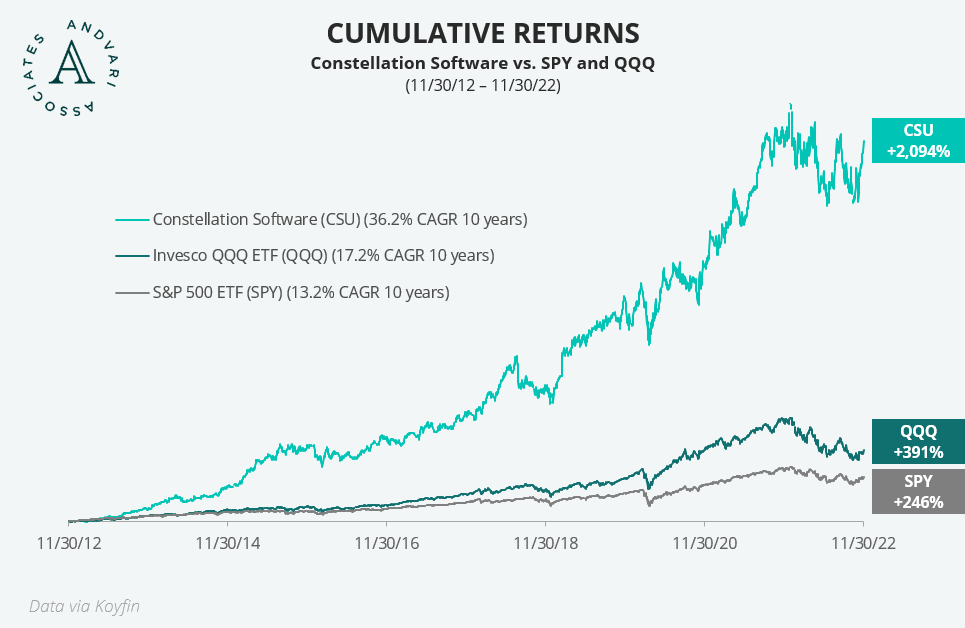

Turning to some positive news, Andvari’s best performing holding in 2023 was Constellation Software whose stock had a total return (share price and dividends) of 58.9%. Constellation’s spin-offs, Topicus.com and Lumine, also had stellar years. In just twelve months, Constellation acquired over 100 niche, vertical market software businesses. Most of the acquisitions were small enough that the purchase price was not reported. However, there were several large transactions in 2023 where Constellation was able to allocate hundreds of millions of capital.

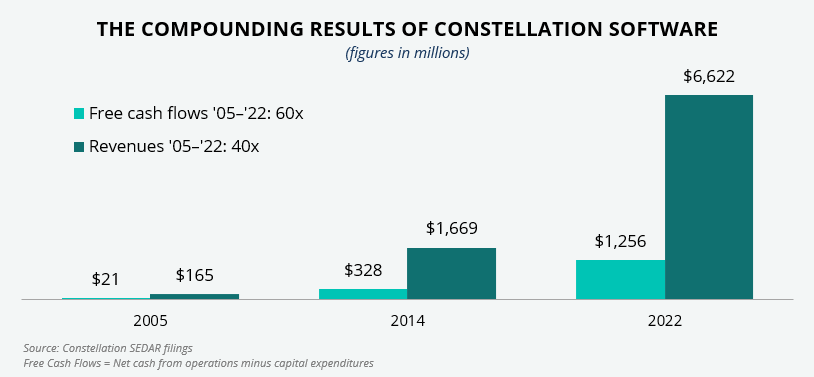

To demonstrate the solid growth and compounding of Constellation’s results, it was just 7 years ago in 2016 that the company first reported annual revenues of $2 billion. Starting with the second quarter of 2023, Constellation reported $2 billion of revenues for a singlequarter. Although Constellation has not yet reported its results for 2023, Andvari believes annual revenues will be at least $8.2 billion and free cash flows will be about $1.7 billion.

Because the businesses Constellation acquires usually have high margins and low organic growth, Constellation is not able to fully reinvest the cumulative free cash flows back into the businesses it owns. Thus, much of the intrinsic value of Constellation is dependent upon its ability to reinvest these free cash flows at high rates of return by acquiring more mission critical software businesses around the world.

As Constellation has grown larger, it has continued to produce excellent results by maintaining its decentralized operating structure. Constellation founder and CEO Mark Leonard has also pushed down capital allocation responsibilities further and further down to business unit leaders. Whereas ten years ago Leonard and the board of directors would be approving nearly every proposed acquisition, business unit leaders now decide for themselves whether to pursue an acquisition if the purchase price is below a certain threshold. Leonard and the board of directors now only consider large acquisitions. This delegation of responsibility has allowed Constellation to deploy capital at a sustained and rapid pace.

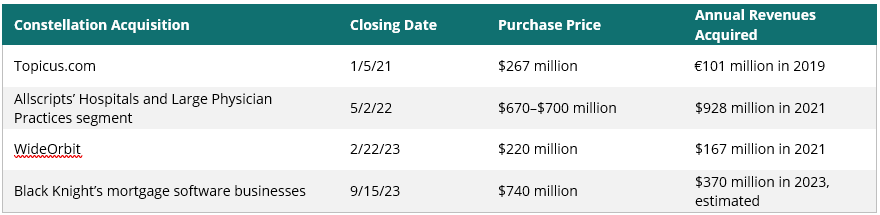

Finally, it’s important to note Constellation’s acquisition criteria have evolved slightly to enable the acquisitions of larger businesses while maintaining a relatively high hurdle rate for returns. Small acquisitions have been Constellation’s bread and butter for decades. Average returns on these have been 20% or higher. But to be competitive in large deals that have a purchase price of $100 million or more, Constellation has conceded it must accept a return in the mid-teens. This is still quite high by the standards of any investor. As shareholders, we’ve seen a handful of larger deals come to fruition in the last several years. Some examples are in the table below.

In sum, Constellation remains an impressive business. Andvari estimates Constellation is currently trading at a forward free cash yield of just under 3%. This, coupled with a track record of having compounded free cash flows at an annualized rate of 18.8% over the last eight full fiscal years, suggests future returns to shareholders are likely to remain above average even if free cash flow growth declines to the low teens.

ANDVARI TAKEAWAY

We’re pleased to report positive results for 2023, but Andvari is still unhappy to be trailing one of the best-known benchmarks, the S&P 500. As unpleasant as it is for us, we must expect this to happen from time to time. To achieve differentiated results, it makes sense to us that we must act differently. Nearly half of Andvari’s assets under management are not part of the S&P 500 index. Furthermore, we run a concentrated investment strategy which can exacerbate results in the short-term.

As always, Andvari does its best to remain focused on what we can control. And that is identifying and studying high quality businesses with excellent managers that can deploy capital at high rates of return for a long period of time. Buying shares of these businesses at sensible prices skew the odds in our favor of producing excellent returns over the long-term for ourselves and for our clients.

As always, I love to hear from clients and anyone else. Please contact me with your thoughts, comments, or questions.

Sincerely,

Douglas E. Ott, II

DISCLOSURES AND END NOTES

* Andvari performance represents actual trading performance of all, actual clients beginning on 4/12/13, managed under the primary Andvari investment strategy. Performance from 12/31/12 to 4/12/13 is actual performance of proprietary accounts, namely the accounts of Andvari’s principal, Douglas Ott. Andvari believes including Ott’s performance figures for the first 4 months and 12 days of 2013 is fair as he managed those accounts similarly to Andvari’s first clients. All performance, including the initial proprietary period, are net of management fees—assumed to be 1.25% per annum, paid quarterly, as currently advertised—net of brokerage commissions and expenses, time-weighted, and includes all cash and other securities. Performance includes realized and unrealized returns and excludes the effects of taxes on incurred gains or losses. Andvari does not certify the accuracy of these numbers. Performance data quoted represents past performance and does not guarantee future results.

The index ETFs are listed as benchmarks and are total return figures and assumes dividends are reinvested. The S&P 500 ETF (SPY) is an exchange traded fund based on the S&P 500 index, which is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. The Russell 2000 ETF is an exchange traded fund based on the Russell 2000 Index, which is an index of 2,000 U.S. small-cap stocks. It is not possible to invest directly in an index. Because Andvari client portfolios are non-diversified, the performance of each holding will have a greater impact on results and may make them more volatile than a more diversified index. Andvari also engages or may engage in strategies not employed by the S&P 500 or the Russell 2000 including, without limitation, the use of leverage.

One may request a list of all securities mentioned or recommended for the preceding year as of the date of this letter. You may contact Andvari using the information below. Actual client results may differ from results depicted in this letter. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the loss of principal. Investment strategies managed by Andvari Associates LLC may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

The discussion of Andvari’s investments and investment strategy (including, but not limited to, current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the views and opinions of Andvari’s portfolio managers and Andvari Associates LLC, the investment adviser, at the time of this report, and can change without notice.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all of Andvari’s forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties, and other factors, most of which are beyond Andvari’s control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.

Andvari's Chief Investment Officer, Douglas Ott, recently recorded a new episode of the Preferred Shares podcast on the history of Orkin, the pest control business owned by publicly traded Rollins, Inc. It's an amazing story about a young immigrant from Latvia who started a business selling rat poison door-to-door in 1901 at the age of 14. Otto grew the business through two world wars and a Great Depression and turned Orkin into the largest pest control business in the world by the 1960s. Otto's children would sell Orkin to Rollins in 1964 for $62.4 million in the first-ever leveraged buyout in corporate history.

Although Otto lacked an education, he had an abundance of energy, tenacity, and business savvy. Otto would soon take full advantage of the power of advertising and marketing, but he focused first on creating a great product and a great service. Otto once said, "I wasn't very good at speaking the English language. But when my customers saw what my products could do, it did my speaking for me."

When it was time to expand beyond the rural Pennsylvania farm upon which he grew up, he would choose Richmond, VA, and then Atlanta, GA, to locate Orkin headquarters. He chose both cities for the same reason: both growing and with no established pest control business. Otto instinctively knew to go where there was no competition!

When it came to advertising, Otto started with telephone books, dabbled in radio, and then hit gold with a series of 20-second spots for television in the early 1950s. This was an animated series depicting "Otto the Orkin Man" (a spray gun) doing battle with other characters such as Legs the Roach and Rags the Rat. Each spot would conclude with a victorious Otto singing a jingle to the tune of "Popeye the Sailor Man".

Image via December 16, 1957, Television Age

Young kids were hooked when they saw these ads. They loved the ads so much that parents would use it as a bribe to get them to go to bed. Orkin would also receive hundreds of fan mail every year from children.

More importantly, the ads were extraordinarily effective for adults. The company shared that tests in several of the 300 cities in 26 states where Orkin has offices showed nearly 70% of unsolicited calls were the result of its TV advertising. The ads were instrumental in increasing Orkin's sales to $12.3 million in 1954, a doubling in less than three years.

We heartily recommend listening to the full conversation about Orkin where the hosts go over all the above, and much more. Just follow this link to the Preferred Shares podcast, where you'll also find a transcript, charts, graphics, and links to resources and additional reading.

IMPORTANT DISCLOSURE AND DISCLAIMERS

Investment strategies managed by Andvari Associates LLC ("Andvari") may have a position in the securities or assets discussed in this article. At the time of publication of this blog, Andvari clients had a position in Rollins. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This document con

Recently, Andvari’s founder and Chief Investment Officer, Douglas Ott, discussed Mars Incorporated in a Preferred Shares podcast. Preferred Shares was created in partnership with Lawrence Hamtil (co-founder and principal at Fortune Financial Advisors) and Devin LaSarre (author of the Invariant newsletter). The podcast explores the forgotten and lesser-known subjects of business, history, and business history.

In this latest episode, Douglas, Lawrence, and Devin discuss the history of Mars, its culture of quality and excellence, its extreme secrecy, how and why it got into the pet food and pet care business, and many other interesting anecdotes. Below is an edited transcript of a portion of the podcast where we discuss the corporate culture of Mars Inc.