A 2016 Harvard Business Review article stated the following about the value of corporate transactions:

M&A is a mug’s game: Typically 70%–90% of acquisitions are abysmal failures.

For what it’s worth, the author also noted that his data was backed by ‘nearly all studies’. Indeed, many disciplined investors feel the hair on the back of their necks stand-up when a beloved company announces plans to grow by acquisition. But not all M&A is destructive. Facebook has Instagram, Google has YouTube and Android, Disney has Pixar and Marvel, and so on.

Exception(s) to the Rule

Within all industries there is the opportunity for companies to acquire their competitors or other companies in related markets. Some may naturally be better at it than others. Andvari acknowledges that M&A is unlikely to add value, yet we hesitate to say “all M&A” is bad. If a management team has the skills and track record of creating value through M&A, it’s a rare thing worthy of attention. Enter Constellation Software (CSU:CN), a brilliant example of a company that has become the acquirer of choice for owners and founders of software businesses.

Creating a Competitive Advantage

Founded in 1995 and public since 2006, Constellation’s pitch to owners of software businesses is simple and mutually beneficial. In exchange for being the ideal “permanent home” of an owner’s business, Constellation will buy the business at a lower-than-average price. The owner, although they won’t receive as much for their business, knows Constellation will take a hands-off approach to the business they spent decades building. No massive employee lay-offs and little meddling. In contrast, other buyers of businesses (like private equity groups) will offer a much higher price and then engage in severe cost-cutting measures after the transaction to fund the purchase. We believe Constellation’s approach gives them an “edge” in buying good businesses and a powerful reputation.

The opportunity for a company like Constellation to offer a permanent home to founders of software businesses remains large. The company has a database of thousands of businesses it would like to buy. Constellation’s CEO, Mark Leonard, has said their most favorite acquisitions are the businesses they buy from founders because “When a founder invests the better part of a lifetime building a business, a long term orientation tends to permeate all aspects of the enterprise.”

Target Hunting

An example of the type of company that would interest Constellation is the still-private Esri, the dominant provider of software that makes digital maps for enterprise clients. Esri was founded in 1969 by Jack Dangermond with $1,100 and now has over $1.5 billion in annual revenues. Dangermond has never taken outside capital, is still running the business, and has said many times Esri will never go public. Talking about the advantage of being private and independent, Dangermond has said:

That means we can concentrate on what our customers want—not what the stockholders or the VCs want. That’s a strategic advantage. Customers notice that we are actually here to support them. And their needs help us innovate. We spend about a quarter of our annual revenue on innovation—about twice what a normal public company spends.

With a commitment to being a place where owners can see their business continue in accordance with the values that made them successful in the first place, Constellation has the “permanent home” advantage over private equity buyers. If Dangermond ever decided to sell Esri, it would be to an owner like Constellation that would allow Esri management to continue running their business as they see fit.

Total Shareholder Returns

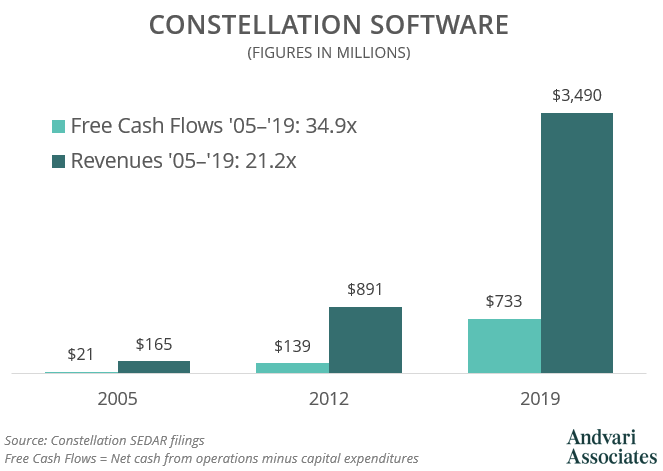

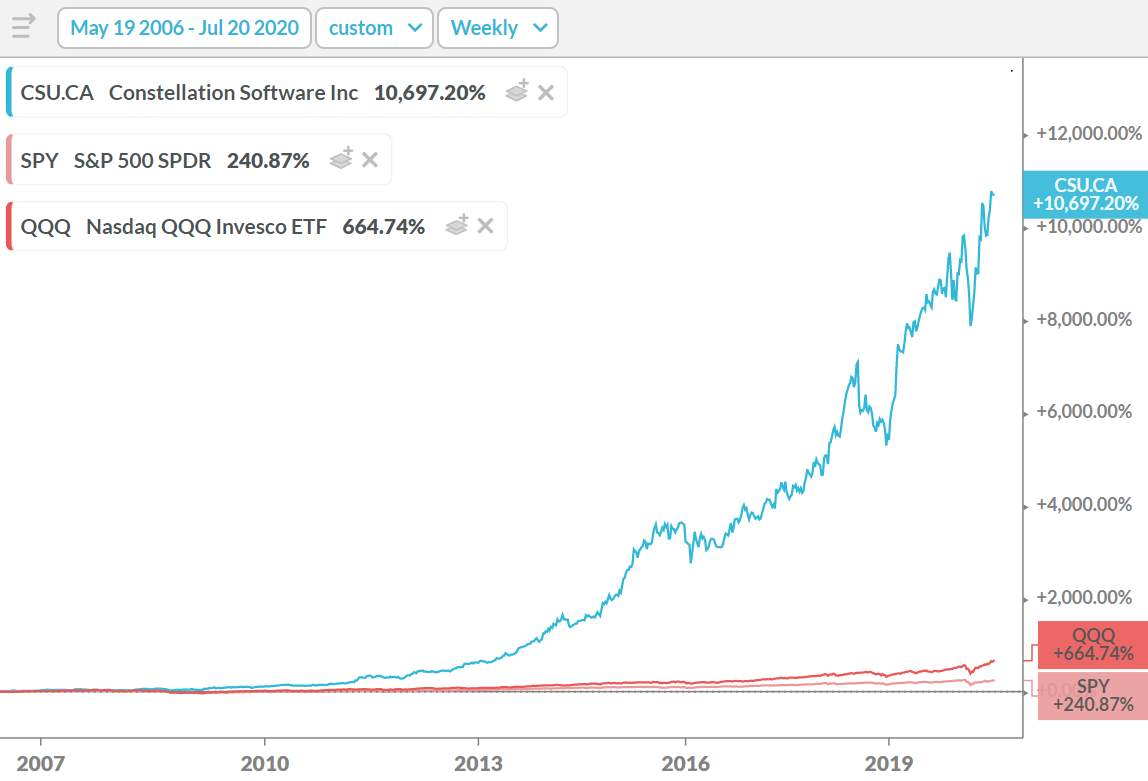

As a result of its “permanent home” approach to M&A, Constellation has a business advantage that has translated into tangible results. From 2005 to 2019, Constellation has grown revenues from $165M to $3,490M (an annualized growth rate of 24.3%) mostly by acquiring over 100 companies. Free cash flows grew at an even faster annualized rate of 28.9%. They’ve done this with barely any debt on their balance sheet, without issuing any new shares, and while maintaining its return on invested capital in the high 20s and low 30s. Constellation’s share price has followed their incredible financial results.

Andvari’s Takeaway

Andvari is always on the lookout for companies like Constellation that have unique and enduring qualities. Constellation’s “permanent home” approach to M&A, coupled with outstanding management, is powerful for two reasons. First, it has contributed to exceptional financial and shareholder returns. Second, it is an advantage that is difficult to replicate by a competitor because it is the outcome of over two decades of networking and reputation-building. Constellation has become known as the Berkshire Hathaway of software because it has the results to be worthy of such a comparison.

-

_________

--

ANDVARI NEWSLETTER

Once every two weeks, Andvari shares insights on great companies, exceptional leaders in business, and related topics in a digestible email format. Click here to sign-up.

-

IMPORTANT DISCLOSURE AND DISCLAIMERS

Investment strategies managed by Andvari Associates LLC ("Andvari") may have a position in the securities or assets discussed in this article. Andvari may re-evaluate its holdings in such positions and sell or cover certain positions without notice.

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This document contains information and views as of the date indicated and such information and views are subject to change without notice. Andvari has no duty or obligation to update the information contained herein. Past investment performance is not an indication of future results. Full Disclaimer.

© 2020 Andvari Associates LLC