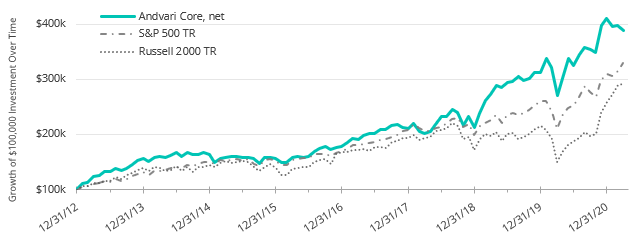

For the first quarter of 2021 Andvari is down 5.2% net of fees while the S&P 500 is up 6.2%.[i] Andvari clients, please refer to your reports for your specific performance figures. The table below shows Andvari’s composite performance against two benchmarks while the chart shows the cumulative gains of $100,000 investments.

ANDVARI HOLDINGS

Although many of our current holdings outperformed the market in 2020 and over the last three years, nearly all these same holdings have underperformed the market in the first quarter of 2021.

Our largest and longest-held position of Charter Communications (via Liberty Broadband and the former GCI Liberty/Liberty Ventures) was down 6% during the quarter. Another large position was down 15%.

After two years of solid performance, a reversal of results like this in the short-term was (and will continue to be) inevitable. We do not spend much time dwelling on it, because these results are a direct outcome of Andvari’s investment philosophy and process.

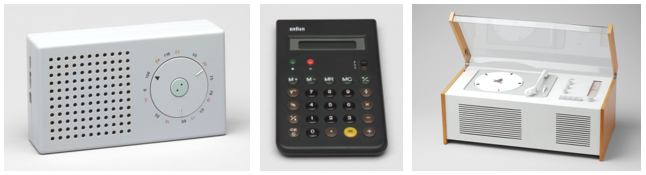

Core to our philosophy is our desire to concentrate capital into our best ideas. As we continue to do so, we expect to experience occasional bouts of underperformance. However, we also expect to use these moments to improve the overall quality of the portfolio at the same time. To help illustrate our thinking, we look to Dieter Rams.

OMIT THE UNIMPORTANT

Dieter Rams is the famous German industrial designer that headed product design for consumer products company Braun from 1955 to 1997. Rams designed products ranging from radios and turntables to calculators and watches. Rams’s designs are simple, functional, and timeless.

Expounding on his approach to design, Rams said, “One of the most significant design principles is to omit the unimportant in order to emphasize the important.” With perfect succinctness, Rams further summarized his approach: “Less, but better.”

FEWER, BUT BETTER

When Andvari started in 2013, the number of companies in client portfolios ranged from 18–20. At the end of March 2021, Andvari is down to 13 names. We’ve learned through experience that simplicity best suits Andvari.

We aspire to have a portfolio of “fewer, but better” businesses. This simplifies our operations and frees up time to spend on more consequential endeavors. Finally, a “fewer, but better” approach should further increase the odds of outperforming the market over the long term at the expense of occasional periods of underperformance in the short term.

CHANGING RATES

In addition to concentration, another feature of our investment process is seeking out and investing in high quality businesses at fair prices. We like companies that sell highly desirable or necessary products. This allows them to raise prices every year without losing customers. We like companies with predictable revenues. This enhances management’s ability to plan for the future and invest accordingly. We like management teams who are motivated to build great businesses with outstanding cultures, not motivated solely to amass a personal fortune. This increases the odds that management treats shareholders like partners and that everyone benefits as the business grows. We want to own these businesses for years, if not decades.

Given the rarity of a wonderful business, it is also a rarity to find one trading at a “cheap” price. They trade at high multiples to their earnings and revenues for good reasons. With interest rates having declined over the years, these high quality companies have become more and more valuable. Consequently, when interest rates rose during the first quarter, this was a factor in the share prices of these companies falling back to earth a bit.

TO COMPOUND UNINTERRUPTED

Andvari does not have the ability to predict where interest rates will be one year from now or five years from now. We cannot time the market to avoid a period where our portfolio might underperform. Instead, we continue our research to understand the growth and reinvestment prospects of great businesses. In periods of volatility, we do our best to make informed decisions.

Selling out of a great business because it reaches a price target or because it might underperform in the short-term is usually a bad decision. As Charlie Munger (Warren Buffett’s long-time business partner and Vice Chairman of Berkshire Hathaway) would remind us, the first rule of compounding is to never interrupt it unnecessarily.

ANDREW FLORANCE & COSTAR GROUP

Moments of volatility within a portfolio like Andvari’s regularly prove opportune. We indeed took advantage of the volatility during the quarter to concentrate our book further. Andvari sold three holdings and reinvested the proceeds back into several other current holdings with better prospects. CoStar Group is one of those current holdings to which we added.

Andvari is attracted to CoStar because it is a great business with an amazing founder. Andrew Florance founded the company in 1987 at the age of 23 and is still the CEO. Florance has an inspiring life story and an envious track record of success. We strongly believe Florance is a person of integrity who measures himself with an internal yardstick rather than an external one. This is important to Andvari as he is far more likely to prioritize building a phenomenal company rather than maximizing his personal wealth at the expense of shareholders.

HUMBLE BEGINNINGS

In a 2019 commencement speech to Virginia Commonwealth University graduates, Florance shared his life story. At the age of seven, he was homeless and had missed more than two years of school. In 1971, the Richmond police took custody of Andy away from his mother. That was the last time he would see her.

Florance overcame this unfortunate starting point with help from others, education, luck, and a lot of hard work. At age 11, he was making enough money to support himself. By age 12 he had applied to and gotten into a music school in New York City. He learned to strive for perfection and to loathe mediocrity. “Getting closer to perfection is a joyous experience,” said Florance.

At school Florance taught himself how to code on a computer. After college, he wanted to use the money he had made on programming jobs to buy and renovate abandoned buildings. However, he became frustrated with the lack of data on properties. Thus, he used his programming skills to develop a commercial real estate (CRE) data service. He founded Realty Information Group (later renamed CoStar) in 1987 to pursue this mission.

HOLDING OUT FOR MORE

After a year or so of grinding out 120-hour work weeks for a meager existence, Florance received an offer to buy his business for half a million dollars. He was inches away from selling the business, but the lawyer he had hired convinced him not to sell. This lawyer believed in the vision of a 23-year-old and invested every dollar he had or could borrow into Florance’s company. The lawyer even took out a second mortgage without telling his wife.

The decision to not sell and to accept investor capital ultimately proved to be the right one. CoStar Group now has revenues of $1.6 billion and a market valuation of over $30 billion.

THE BUSINESS OF COSTAR

CoStar has two businesses, their original CRE information business and their online marketplace business. The information business collects and maintains property level data in major real estate markets. The brokerage firms back then all had in-house departments that collected data. This was a time- and money-consuming effort that was not core to the business of leasing and transacting real estate for clients.

Florance saw that a single company collecting data could eliminate the duplicative in-house efforts, provide the data at a lower total cost, and earn high margins for itself at scale. The CoStar Suite of products is now the industry standard with 93% of the top 1,000 brokerage firms as clients.

Online marketplaces are CoStar’s second business. If you’re an owner of multifamily apartments, your best option to lease up your units is to advertise through CoStar’s Apartments.com web site. If you have commercial property or rural land to sell or lease, the best place to go is CoStar’s LoopNet and LandsofAmerica. These online sites have extremely high profits because they are beneficiaries of network effects. They have the largest amount of web traffic which attracts more advertising dollars. For example, LoopNet has 20x the monthly web traffic of its next closest competitor.

CoStar estimates the total value of commercial real estate across the globe is $66 trillion. CoStar’s data and services are essential for the lease, sale, and valuation of CRE properties. With $1.6 billion in revenues, CoStar is still a small service provider in the grand scheme. The company has room to grow significantly over the next 10 years.

They are still at the beginning stages of building out their CRE data business in Europe. With their apartment listing service in the U.S., there is a massive opportunity to increase their 3% penetration of the 350,000 apartment communities with 5 to 100 units. Finally, we expect CoStar’s already high margins will continue to expand over time.

ANDVARI TAKEAWAY

Andvari has taken a steady approach to the evolution of our investment approach and process. The quality of businesses in our portfolio and our watchlist have improved. We’ve learned to let winners run and to cut losers sooner rather than later. We’ve learned that, in general, simplicity is better than complexity. “Fewer, but better.”

We don’t enjoy trailing the market in the short term, but we know this is the price we pay for increased odds of above average performance over the long term.

As always, I love to hear from clients and interested parties about anything on your mind. Please contact me with your thoughts, comments, or questions.

Sincerely,

Douglas E. Ott, II

-

_________

-

IMPORTANT DISCLOSURE AND DISCLAIMERS

The opinions expressed herein are those of Andvari Associates and are subject to change without notice. Past performance is not a guarantee or indicator of future results. You should not consider the information in this communication a recommendation to buy or sell any particular security. You should not assume any of the securities discussed in this report are or will be profitable, or that recommendations we make in the future will be profitable. Consider the investment objectives, risks, and expenses before investing.

[i] Andvari performance represents actual trading performance of all, actual fee-paying clients beginning on 4/12/13. Performance from 12/31/12 to 4/12/13 is actual performance of proprietary accounts, namely the accounts of Andvari’s principal, Douglas Ott. Andvari believes including Ott’s performance figures for the first 4 months and 12 days of 2013 is fair as he managed those accounts similarly to Andvari’s first clients. All performance, including the initial proprietary period, are net of management fees (assumed to be 1.25% per annum, paid quarterly, as currently advertised), net of brokerage commissions and expenses, time-weighted, and includes all cash and other securities. Performance includes realized and unrealized returns and excludes the effects of taxes on incurred gains or losses. Andvari does not certify the accuracy of these numbers. Performance data quoted represents past performance and does not guarantee future results.

The indexes are listed as benchmarks and are total return figures and assumes dividends are reinvested. The S&P 500 Total Return Index is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. The Russell 2000 Index is an index of 2,000 U.S. small-cap stocks. It is not possible to invest directly in an index. Because Andvari client portfolios are non-diversified, the performance of each holding will have a greater impact on results and may make them more volatile than a more diversified index. Andvari also engages or may engage in strategies not employed by the S&P 500 or the Russell 2000 including, without limitation, the use of leverage.

One may request a list of all securities mentioned or recommended for the preceding year as of the date of this letter. You may contact Andvari using the information below. Actual client results may differ from results depicted in this letter. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the loss of principal.

The discussion of Andvari’s investments and investment strategy (including, but not limited to, current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the views and opinions of Andvari’s portfolio managers and Andvari Associates LLC, the investment adviser, at the time of this report, and can change without notice.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all of Andvari’s forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties, and other factors, most of which are beyond Andvari’s control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.