We are pleased to share a summary version of a recent research report we compiled on Tyler Technologies (TYL), a business that embodies several of the intangible business qualities we seek at Andvari. Access to the full, 14-page thesis is available through our client document portal. If you would like access to the portal or the individual report, please contact Info@AndvariAssociates.com.

Executive Summary: Boring But Beautiful

Tyler Technologies is the only public company focused on software for state and local governments in North America. Since 1998, Tyler has acquired over 40 software companies and revenues have grown from $50 million to over $1 billion. Cash flows and operating profits have grown at faster rates. Shareholders have benefited greatly.

The company has many qualitative attributes that have driven past success, a number of which we highlight below. Looking to the future, Tyler’s markets have grown at 7%–8% while Tyler itself has grown at 1.5x to 2.0x the market. This growth rate is still achievable going forward given Tyler’s expanding suite of products. Margins are in the mid-20s and can grow into the mid-30s over the next decade. Margins are currently low because Tyler has been investing heavily to enhance its offerings to win more and larger clients.

Although current valuation multiples appear high (a characteristic that importantly does not inhibit Andvari from digging deeper on a name), there are decades of revenue growth and margin expansion ahead for Tyler. Andvari expects Tyler will provide us with annualized returns of 12% over the next 10 years at current prices.

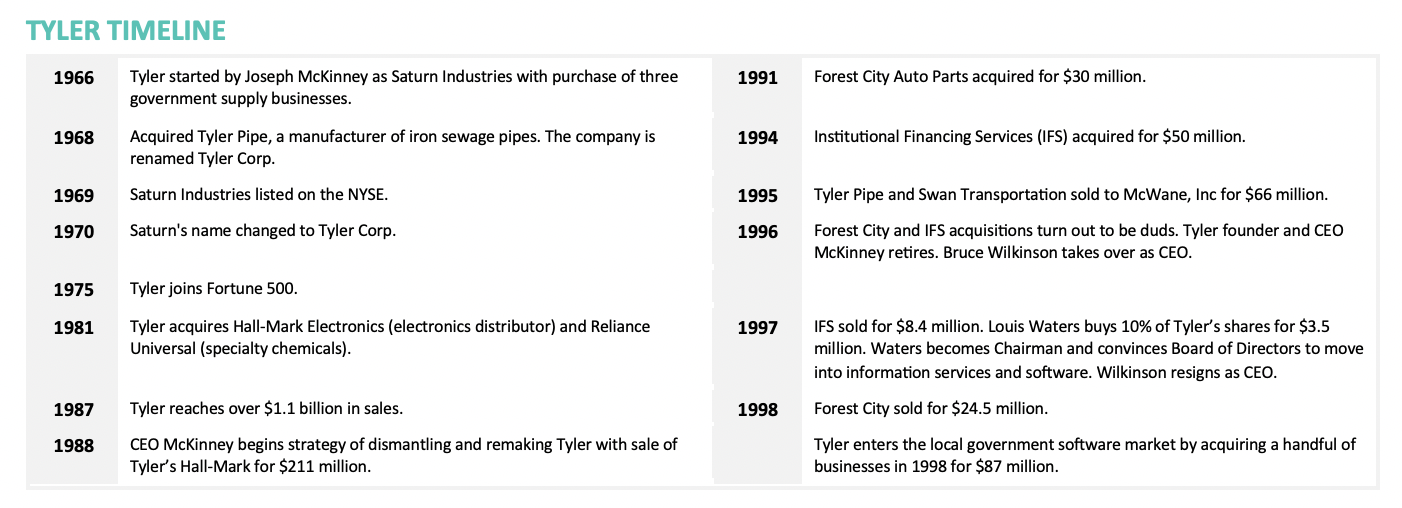

History of Tyler Tech

Although Tyler is now a pure software company, it started out as a manufacturing and industrial company. Joseph McKinney, a venture capital investor in the 1960s, used his early financial success to start a company named Saturn Industries. McKinney acquired Tyler Pipe in 1968, a manufacturer of sewage pipes, and changed Saturn’s name to Tyler Corporation. Until the late 1980s, McKinney used Tyler as a vehicle to acquire multiple businesses.

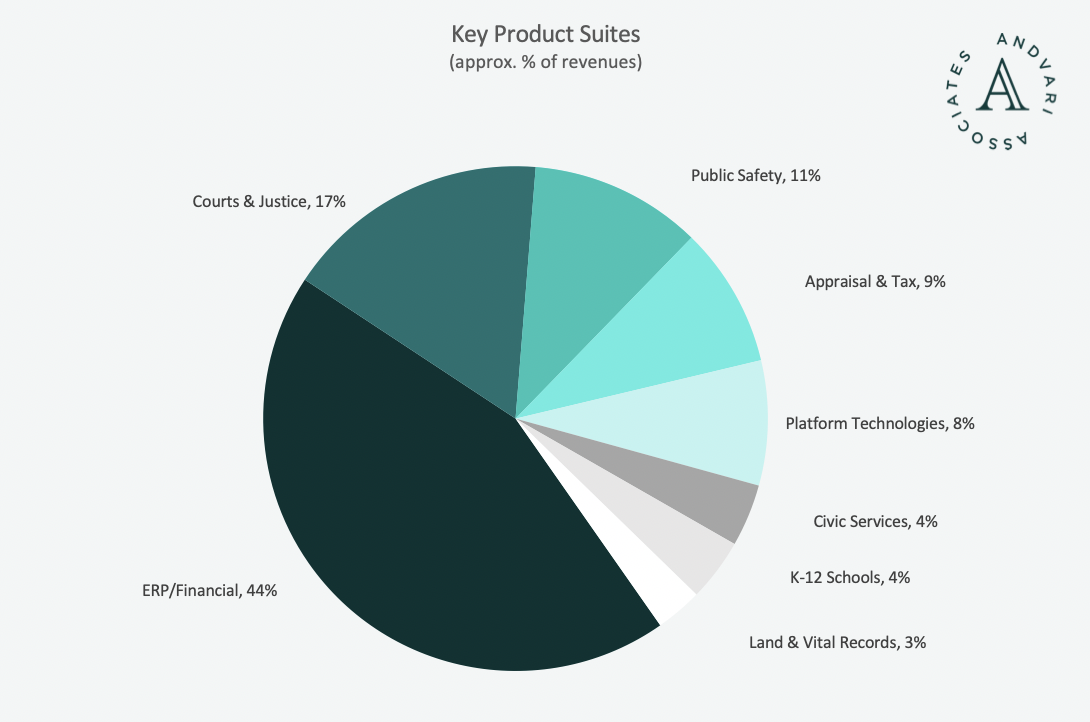

Tyler Tech Today

Tyler is diversified by product suite and has over 26,000 installations of their products currently in place. ERP/Financial products make up 44% of total revenues, Courts & Justice products make up 17%, and Public Safety 11%. These three add up to 72% of revenues.

Key Andvari Attributes

Tyler has multiple features that make it a high quality and extremely valuable business. We summarize 5 of the company’s key strengths below. The full report contains a total of 9 such attributes, The full report contains a total of 9 such attributes, plus adds substantial depth of discussion to each respective attribute.

- Highly Fragmented Markets - In addition to the 50 states, there are roughly 3,000 counties, 36,000 cities and towns, and 13,600 school districts. There also are 35,000 local agencies. Each government has their own systems: tax systems, court systems, land record systems, enterprise resource planning systems, etc. Gartner Research estimates the total spend by the local government sector on software is $20 billion each year. Tyler’s products address $10 of that $20 billion. With $1 billion in revenues, Tyler has about a 10% market share.

- Niche Market Domination - Tyler operates in a collection of small, niche markets focused exclusively on the needs of governments customers. Government business processes are different from corporate processes. And there are multitudes of differences between local governments. This requires a high level of intimacy with the customer. Tyler’s products have gained significant market share as a result, and broadly, we like companies that dominate niches.

- High Customer Retention & Revenue Predictability - Tyler has customer retention rates of almost 99%. Once a local government becomes a Tyler customer, they can be there for life. St. Louis County is a good example of a long-time client and the potential of new Tyler clients. The county has been a client of Tyler’s Appraisal and Tax solution since 1981. Then the county bought Tyler’s appraisal software in 1998, Tyler’s assessment software in 2003, and then Tyler’s municipal court case management solution in 2008.

- High Quality and Aligned Management - Management is high quality. They are focused on the next several decades and have acted accordingly. They are willing and able to reduce margins to reinvest in the business. Management has also been opportunistic repurchasers of Tyler shares. Compensation incentives are reasonable and aligns management to grow shareholder value over the long-term.

- Adept Capital Allocation - Management has allocated capital well over the years. They have acquired over 40 software companies (a skill we value) and have reinvested in their businesses. Regarding share repurchases, Tyler has been opportunistic and successful.

Key Risks to Our Thesis

- Margins - Margins do not expand as management has promised. Chances are low here. Tyler still has runway for decades of growth. Tyler is not even close to being a mature software company. Tyler’s management has historically done what it says it will do.

- Organic Growth Weakness - Organic growth takes an extended hit. Tyler’s sales growth has recently decelerated due to local governments delaying upgrades and projects. Tyler’s fair value and forward returns will take a big hit if future growth is permanently impaired.

- Bad M&A - Management makes bad acquisitions. If Tyler starts to acquire companies simply to consolidate market share, Andvari would become concerned.

Andvari Takeaway

Tyler Technologies possesses many qualities that make for a high quality business. The first (and often loudest) criticism we hear about Tyler is related to Valuation. We agree it does have optically high valuation multiples based on current financials. There is also a narrow gap between Andvari’s estimate of fair value and market value. However, these facts mask the opportunity to earn good returns by investing in Tyler. At Andvari, we frequently emphasize that ‘expensive-looking’ stocks aren’t necessarily bad investment opportunities. This is often a function of one’s investment horizon, which, for us, is indisputably long.

We believe Tyler remains far away from its true, underlying earnings power. Margins can expand into the 30% and even 40% range over time. The opportunity for long, steady growth remains large: Tyler only has 10% of a current TAM of $10 billion. Its market share will only go higher as they land and expand with customers that can be with Tyler for life. Andvari is confident Tyler will grow its intrinsic value at low double-digit rates over the long-term and that we as shareholders will consequently earn similar annualized returns.

As a reminder, access to the full, 14-page thesis is available through our client document portal. If you would like access to the portal or the individual report, please contact Info@AndvariAssociates.com.

-

_________

--

ANDVARI NEWSLETTER

Once every two weeks, Andvari shares insights on great companies, exceptional leaders in business, and related topics in a digestible email format. Click here to sign-up.

-

IMPORTANT DISCLOSURE AND DISCLAIMERS

Investment strategies managed by Andvari Associates LLC ("Andvari") may have a position in the securities or assets discussed in this article. Andvari may re-evaluate its holdings in such positions and sell or cover certain positions without notice.

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This document contains information and views as of the date indicated and such information and views are subject to change without notice. Andvari has no duty or obligation to update the information contained herein. Past investment performance is not an indication of future results. Full Disclaimer.

© 2020 Andvari Associates LLC