When faced with the choice between a company with increasing cyclicality and higher balance sheet risk or a company with decreasing cyclicality and lower balance sheet risk, what prudent investor/capital allocator wouldn’t choose the latter? Yet all too often we see good businesses consciously drifting toward the former.

Large, growing markets present obvious appeal to business leaders and investors, but the pursuit of these shiny objects can be fraught with risks of lost time and money. The scenario reminds us what specific behaviors we value in our executives.

Optionality as Risk

An example of this is playing out right now in the markets for online real estate listing. Enter Zillow and CoStar Group, giants of the residential and multi-family/commercial niches, respectively. Soon after Zillow announced in April 2018 they would be getting into the home-flipping business with a service called Zillow Offers, CoStar’s founder and CEO Andrew Florance would comment that flipping is an awful business.

“Recently, I think because of [Zillow’s] recent announcement, I field a number of questions as to whether or not we might pivot — begin flipping commercial buildings to drive revenue. I want to be clear. That even after successfully buying our Washington, D.C. company headquarters for $41 million in 2010 and selling it a year later for $100 million of sale-leaseback, we’re not going to become flippers.

We recognize that flipping is a completely different business from building marketplaces or Information Services. It’s lower margin, it’s lower quality revenue and has horrific cyclical and balance sheet risk. Instead, we expect to use our balance sheet and strong financial position to make strategic acquisitions and make sound investments to develop a broad myriad of great high-margin growth opportunities we see ahead of us.”

A Conscious Decision

Although both companies control respectively dominant online platforms for listings (Zillow for residential and CoStar for multi-family and commercial), they are divergent in strategy. Zillow is choosing a much riskier path while CoStar continues on a more certain path. Incredibly, Zillow admits to the unattractive traits of Zillow Offers in its 2019 10-K filing:

“Zillow Offers…is a cash- and inventory-intensive business with a high cost of revenue as compared with other parts of our operations.”

TAM Wagging the Dog

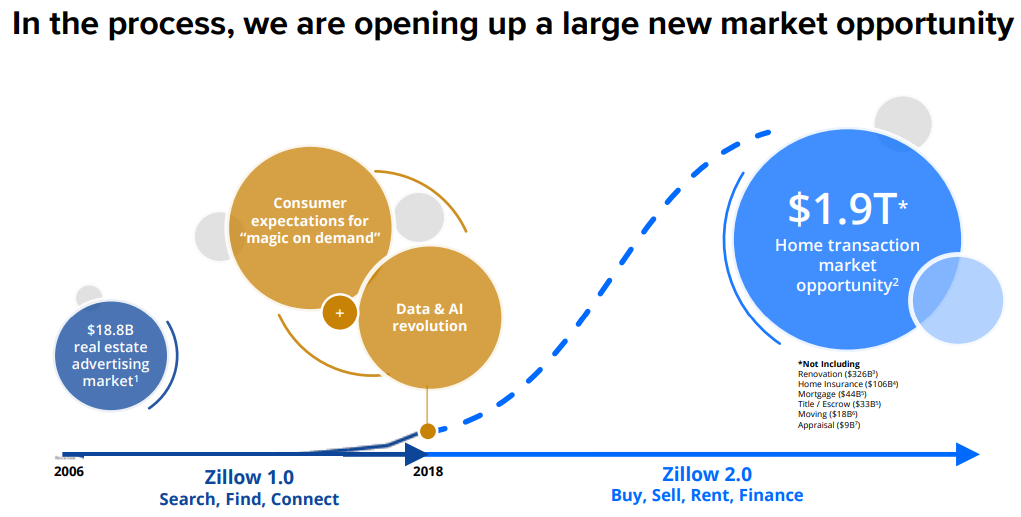

The one reason Zillow has given on why it's getting into the home flipping business is it opens up a huge total addressable market (TAM) of $1.9 trillion (the estimated total transaction value of existing and new homes sold in 2019) versus Zillow’s traditional segment which is a mere $19 billion.

Source: 2020 Zillow Investor Presentation

We believe the real reasons are slightly different. First, Zillow’s growth in its traditional business was slowing dramatically. Second, Zillow then saw the growth of other home-flipping companies and decided it could not concede market share in a new, related market.

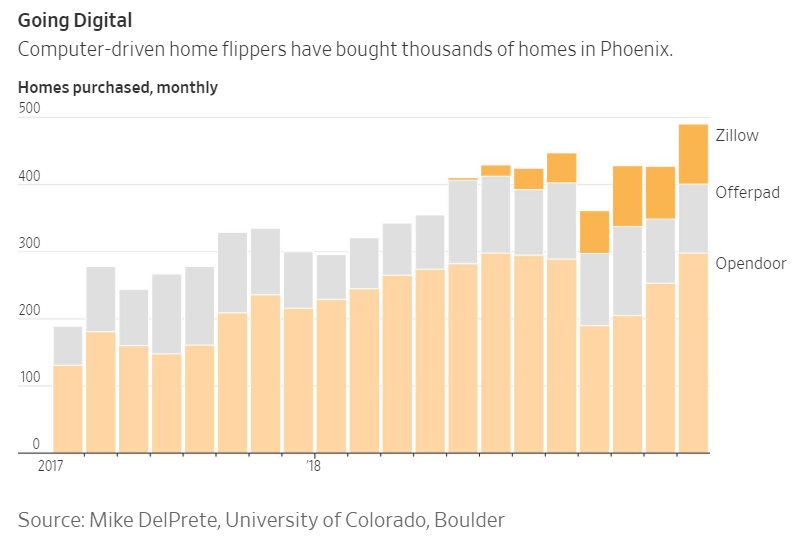

Opendoor and Offerpad have been the leaders in the “iBuying” movement in residential real estate (see the chart below), which is simply where a company makes an immediate cash offer to a home seller with the goal of performing light renovations and flipping the home within a few months. Zillow likely did not want to be left out.

Growth of iBuying in Phoenix, AZ

Andvari likes to see focus in our leaders, and this decision by Zillow is not a trivial pivot to make for a tech business. Zillow has effectively decided to become a real estate speculator.

At the Margin

Regardless of the real reason for Zillow getting into home flipping, Zillow has exposed itself to a bad business. Even if Zillow can turn Offers into a profitable business, Zillow admits EBITDA margins will be a meager 4% at best. Also discouraging is that Zillow lacks control over the main factors that affect its margins. A home might take longer to sell than expected. Renovation expenses do not seem to be scalable. Worst, the real estate market could turn south in a recession.

CoStar has stuck to growing and improving its two core businesses of commercial real estate (CRE) data and online marketplaces. Revenues are predictable and counter-cyclical—CoStar grew revenues 16% during the second quarter of 2020. EBITDA margins are in the upper 20s and can easily go higher over time.

Andvari Takeaway

The correct answer, to us, is obvious. We agree with Andy Florance that flipping real estate, particularly for a tech-oriented platform like Zillow, is a poor use of capital. We also must give kudos to Florance and any other executive that can maintain strategic discipline in the face of tempting, but risky distractions.

In a tug-of-war contest between a high-margin, capital-light, counter-cyclical business (CoStar) and the opposite (Zillow’s new home flipping business), Andvari will side with that CoStar-like business every time. We believe our long-term performance will be better off as a consequence.

-

_________

--

ANDVARI NEWSLETTER

Once every two weeks, Andvari shares insights on great companies, exceptional leaders in business, and related topics in a digestible email format. Click here to sign-up.

-

IMPORTANT DISCLOSURE AND DISCLAIMERS

Investment strategies managed by Andvari Associates LLC ("Andvari") may have a position in the securities or assets discussed in this article. Andvari may re-evaluate its holdings in such positions and sell or cover certain positions without notice.

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This document contains information and views as of the date indicated and such information and views are subject to change without notice. Andvari has no duty or obligation to update the information contained herein. Past investment performance is not an indication of future results. Full Disclaimer.

© 2020 Andvari Associates LLC