Below is our latest letter to clients. Please share and enjoy.

Dear Friends,

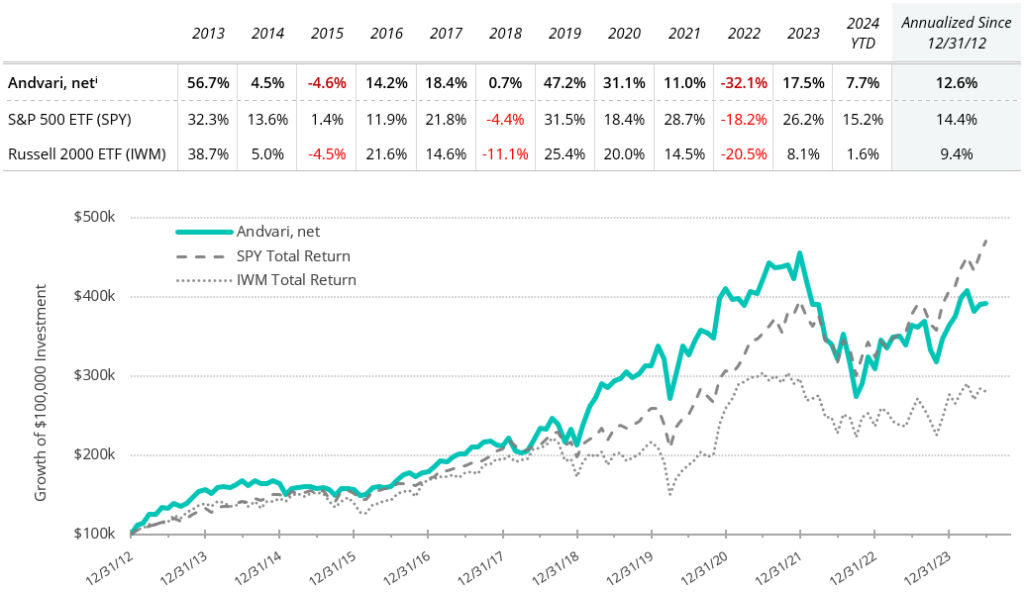

For the first quarter of 2024, Andvari was up 7.7% net of fees while the SPDR S&P 500 ETF was up 15.2%.* Andvari clients, please refer to your reports for your specific performance and holdings. The table below shows Andvari’s composite performance while the chart shows the cumulative gains of a $100,000 investment.

The main reasons for Andvari’s lagging returns are twofold: (1) Andvari has not owned some of the largest and best performing companies such as Nvidia, Apple, Microsoft, Google, Meta, and Amazon; and (2) the poor performance from Mesa. To put Andvari’s performance in better context, it’s important to know we are invested in a wide range of companies in terms of market cap. We’ve owned, or currently own, companies valued at hundreds of millions to billions and tens of billions to hundreds of billions. Given the performance of the small cap Russell 2000 index ETF (up 1.6% for the first six months) and the performance of the large and mega cap S&P 500 index ETF (up 15.2%), it is reasonable that Andvari’s performance is somewhere in the middle at this moment in time.

It’s also worth noting that Andvari’s performance in just the first six months of the year is in line with what the market on average produces in a full year, which is nothing to sneeze at. But when compared only to the higher performance of the large caps, it can feel disappointing.

ANDVARI HOLDINGS

Andvari sold out of two holdings, the largest of which is Mesa. Mesa was one of our longest held investments at the time we sold. It had performed well up until the end of 2021. Unfortunately, we held on too long. Management made two large acquisitions, one before and the other during the COVID era. It eventually turned out they paid too much for both, which does not speak well of their ability to allocate capital.

Mesa later announced in June it would delay the filing of its annual audited financial statements. A significant part of Andvari’s investment thesis was that Mesa could transition from a small-cap company run in a small-cap way to a mid- to mid-cap company run in a more professional manner. After failing to file one of its most important documents in a timely manner, Andvari felt—regretfully—some vindication we decided to cut bait and throw our line out for better fish. Thinking about what Andvari could have done differently, we likely would have made the same investment given what we knew at the time, but we should have made it a smaller position.

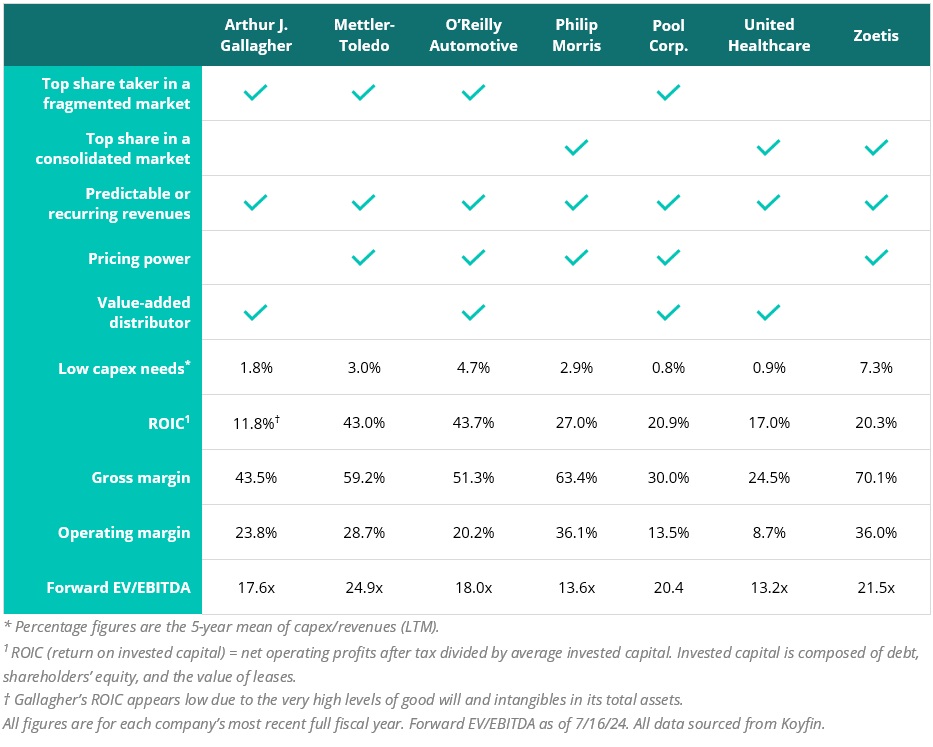

With a large amount of capital to redeploy, we started positions in a handful of companies we’ve followed for years. The table below shows how Andvari views some of the qualitative and quantitative attributes of these companies. We also give a brief overview of each company in the remainder of our letter.

ARTHUR J. GALLAGHER

Founded in 1927 by Arthur J. Gallagher, the eponymous firm is now the third largest retail property and casualty insurance broker in the United States and also the third largest reinsurance brokerage firm in the world. In addition to their brokerage businesses, Gallagher is a significant player in third-party claims administration and HR & benefits consulting.

As hinted in the above table, Gallagher is an acquisitive company. It has been a major consolidator of the highly fragmented market of insurance brokers for decades. In just the past five full years, Gallagher has acquired 195 businesses. And the market still remains fragmented. The company estimates there are tens of thousands of independent firms across the English-speaking countries of the world.

Given Gallagher’s ability to grow organically, grow through acquisition, and the essential services it provides, there have only been three times in the past twenty-five years when revenues declined: down 0.56% in 2005, down 0.31% in 2008, and down 1.63% in 2020. Which is to say, revenues barely budged despite those tumultuous years. This is a resilient company.

METTLER-TOLEDO

Mettler-Toledo makes a variety of lab instruments as well as weighing scales for industrial and retail use. These products are essential to the end users and often required to comply with a variety of regulations. The company has the number one product in most areas where it competes. However, its market share ranges from 25% to 30% share in these business lines. This means, despite its top status, competition remains highly fragmented, which gives them opportunity to capture more share over time.

With an installed base of over $16 billion worth of machines across the world, revenues from services and consumable adds to the predictability of total revenues. Pricing power is strong given the high value and relatively low cost of their products to end customers. Mettler has consistently captured 200 basis points (or greater) of net pricing every year. The company even successfully raised prices during 2009.

O'REILLY AUTOMOTIVE

O’Reilly is the third largest auto parts retailer in the country with over 6,095 stores in North America and Mexico. Their sales are split 60% to people who want to repair their own car and 40% to professionals who fix and maintain cars for a living. Following the common theme, O’Reilly sells essential products that people will buy regardless of the state of the economy.

We love that this business gushes cash—it had an extraordinary return on invested capital of 43.7% in 2023. O’Reilly has also had negative working capital since 2017, which means customers pay O’Reilly before O’Reilly needs to pay its suppliers. Looking at its capex, O’Reilly does have a higher capex ratio when compared to the others in the table. However, the ratio is still quite low considering O’Reilly is growing its store count in the range of 150-200 per year. At this rate, O’Reilly is expanding its store count by about 3% annually. Also driving the recent increase in capex has been a shift towards owning their stores rather than leasing them.

PHILIP MORRIS

Andvari invested in Philip Morris a few months after initiating a position in fellow tobacco company Altria. The tobacco industry is one that has consolidated to only a handful of players. For decades, the industry has more than offset the continual decline in cigarette volumes with price increases. More recently, both Altria and Philip Morris have introduced several new product categories that deliver nicotine in much safer ways: vaping, nicotine pouches, and heat-not-burn products. Nicotine pouches in particular continue to have an extraordinary growth trajectory. In the most recent quarter, the volumes of Altria’s On! pouches and Philip Morris’ Zyn pouches continued their torrid growth rates at 30%+ and 70%+ year over year, respectively.

For Philip Morris and Altria, their margins are high, returns on equity and capital are high, and both trade at what Andvari views as cheap or very cheap multiples. Given the non-zero chance of a “nicotine renaissance” aided by less harmful products, we do not think the future for these companies is as dim as the market seems to think.

POOL CORP

Pool is the largest player in a niche market. They are a value-added distributor of all materials and equipment related to the maintenance, remodeling, and construction of swimming pools. Although they have an estimated 40% market share, the market remains highly fragmented, which means they can grow at an above average rate organically and via further acquisitions.

In general, Pool operates in an industry with good tailwinds. Population migration from the north to the south, primarily by retirees, means more new pools and more remodeling of old pools. As the CEO of Pool recently said, the industry joke is that trucks move north with oranges and move south with furniture. Furthermore, once a home has a pool, this ensures a long-term annuity stream of products used to maintain that pool. These are non-discretionary purchases, because if an owner allows a pool to fall into disrepair, this negatively impacts the value of their home. Thus, Pool can easily pass on price increases to their customers.

As a value-added distributor, Pool is a conduit between over 2,200 manufacturers and over 120,000 customers that maintain and build swimming pools. They have taken on the role of trusted partner to manufacturers and end users. They ensure quick, efficient delivery of products while also minimizing the chances of products being out of stock. They have the largest and widest selection of products. They strive for the best customer service. They can advise customers on the best products to meet maintenance or construction needs. They’ve developed software and apps that make owning and maintaining pools easier. For all this, suppliers and customers have rewarded Pool with their long-term business. And the great part about the business is that pools remain a desirable addition to homes. This ensures a slow yet steady growth in their installed base, which drives non-discretionary, recurring sales.

UNITED HEALTHCARE

United Healthcare is one of the largest providers and distributors of services in the $5 trillion U.S. healthcare market. The company provides services to employers, individuals, and those eligible for Medicare and Medicaid. United’s Optum segment provides pharmacy benefit services and a slate of other insights and services to the major players in the healthcare space: physicians, hospitals, government agencies, and life science companies.

This is a company that provides essential services and has a strong wind at its back. Over two million people are enrolling in Medicare and Medicare Advantage every year. With the increase of healthcare spending every year, the value of the services and insights provided by Optum will only increase. United is a solid business with a high teens returns on its capital. After reinvesting in its businesses, United will likely return $16 billion in 2024 in the form of dividends and share repurchases off a revenue base of ~$380 billion.

ZOETIS

Zoetis was spun out of Pfizer in 2013 and is the largest company serving the animal health market. They make medicines, vaccines, diagnostics, devices, and technology solutions for their pet owners and veterinarians. Their revenues are split 65% for pet care and 35% for livestock.

The nice thing about Zoetis, and the pet healthcare market in general, is the trend of increasing pet ownership and the increasing willingness to spend more money on pets every year. When compared to overall consumer spending, spending on pets has nearly doubled since 1990. The resilience of the pet healthcare industry is particularly exceptional—the industry has never had a year of negative growth in the last 15 years. Zoetis in particular has grown several percentage points faster than the industry.

The financials of Zoetis are also exceptional. It has steady revenue growth, gross margins in the 70s, an ability to reinvest in the business at 20% returns, and is still able to return billions to shareholders with dividends and share repurchases. Despite having the highest ratio of capex to revenues in this group of new holdings, Zoetis is still very cash generative. The company generated $1.8 billion of free cash over the last twelve months off of $8.7 billion of revenues, a healthy 20% margin. In its first five years after being spun from Pfizer in 2013, Zoetis averaged 4.1% of capex to revenues. The reason for capex trending higher over the last five years is to support a slate of fast-growing new products, inventory buildups, and productivity enhancements. We believe this capex ratio will slowly come down over time as revenues come in for its newer products and as customers draw down inventories.

ANDVARI TAKEAWAY

Andvari redeployed capital into a handful of businesses which we believe will produce above average returns over the long term. Although we increased the total number of holdings in the equity portion of client portfolios (most have 21 or fewer individual names), we still maintain a high degree of concentration. Andvari’s top five equity positions continue to account for more than 50% of total assets under management.

With inflation continuing its slow decline, the probability of slightly lower interest rates by year’s end, and the eventual end to the COVID overhang for our life sciences holdings, Andvari expects better performance for many of its holdings over the coming years.

As always, I love to hear from clients and anyone else. Please contact me with your thoughts, comments, or questions.

Sincerely,

Douglas E. Ott, II

DISCLOSURES AND END NOTES

* Andvari performance represents actual trading performance of all, actual clients beginning on 4/12/13. Performance from 12/31/12 to 4/12/13 is actual performance of proprietary accounts, namely the accounts of Andvari’s principal, Douglas Ott. Andvari believes including Ott’s performance figures for the first 4 months and 12 days of 2013 is fair as he managed those accounts similarly to Andvari’s first clients. All performance, including the initial proprietary period, are net of management fees—assumed to be 1.25% per annum, paid quarterly, as currently advertised—net of brokerage commissions and expenses, time-weighted, and includes all cash and other securities. Performance includes realized and unrealized returns and excludes the effects of taxes on incurred gains or losses. Andvari does not certify the accuracy of these numbers. Performance data quoted represents past performance and does not guarantee future results.

The exchange traded funds (ETFs) are listed as benchmarks and are total return figures and assumes dividends are reinvested. The SPY ETF is based on the S&P 500 Index, which is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. The IWM ETF is based on the Russell 2000 Index, an index of 2,000 U.S. small-cap stocks. It is not possible to invest directly in an index. Because Andvari client portfolios are non-diversified, the performance of each holding will have a greater impact on results and may make them more volatile than a more diversified index. Andvari also engages or may engage in strategies not employed by the S&P 500 or the Russell 2000 including, without limitation, the use of leverage.

One may request a list of all securities mentioned or recommended for the preceding year as of the date of this letter. You may contact Andvari using the information below. Actual client results may differ from results depicted in this letter. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the loss of principal. Investment strategies managed by Andvari Associates LLC may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

The discussion of Andvari’s investments and investment strategy (including, but not limited to, current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the views and opinions of Andvari’s portfolio managers and Andvari Associates LLC, the investment adviser, at the time of this report, and can change without notice.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all of Andvari’s forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties, and other factors, most of which are beyond Andvari’s control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.